33

Are Professional Investors Sophisticated? by Lukas Menkhoff, Maik Schmeling and Ulrich Schmidt* Leibniz Universität Hannover, *University of Kiel Presentation at ETH Zürich, 26.11.2008

Are Professional Investors Sophisticated?

by Lukas Menkhoff, Maik Schmeling and Ulrich Schmidt*Leibniz Universität Hannover, *University of Kiel

Presentation at ETH Zürich, 26.11.2008

Motivation for our research

We know that participants in financial makets often show unsophisticatedbehavior: it reduces performance and seems to be avoidable

Examples for such unsophisticated behavior:• Excessive turnover (Dow and Gorton, 1997)• Home bias (Shiller et al., 1996)• Loss aversion (Coval and Shumway, 2005)• Herding (Sias, 2004)

Even more surprising is the fact that professional market participants are notonly subject to such behavior too but that they may be even worse thanlaymen.

On the other hand: some studies show that professionalism is a performance-enhancing factor.Unclear evidence on the impact of professionalismOur contribution: provide another research design which has pros (and cons)

Ways of examining investors‘ sophistication

1. Models of financial markets assume that there are (some) rational, well informed inestors, i.e. sophisticated investors

1. The first way of examination: „real“ trading data of investors, showingwhether they made profits or avoided big mistakes etc.

problem: limited coverage in particular about motivation of decisions orlinkage to personal information etc. (control variables)

2. The second way of examination: experiments are precise as they controlenvironmental conditions

they may be irrelevant if they examine the „wrong“ group (mainlystudents)

3. The third way of examination: collecting survey data from investorsprovides a rich set of information („framed field experiment“)

this comes at the price of precisionThis research provides complementary evidence.

This research contributes to the literature in 4 ways

1. Comprehensive: Sometimes behavioral finance literature is eclectic in that a single phenomenon is analyzed witha given data we analyze 6 measures of sophisticated behavior; 5 of these are the avoidance of biases plus forecasting ability

2. 3 investor groups: if groups are distinguished it is usually betweenprofessionals and laymen we distinguish between 3 groups, i.e. 2 groups of professionals, „institutional investors“ and „investmentadvisors“.

3. Controls: first, variables having impact in the same way as professionalism, i.e. experience, wealth; second, further importantcontrols of financial behavior, such as age, education, attitudes.

4. Less interference: professionals show biased behavior on the job, dueto incentives (low transaction costs, incentives for turnover) so, high turnover of professionals may be caused by low transaction costs lessinterference in the private domain, i.e. we compare the private decisionmaking of the 3 investor groups

Main findings

1. Also professional investors are subject to some degree of biasedinvestment behavior.

2. Professionals are not alike: Institutional investors behave moresophisticated than laymen whereas investment advisors seem to berather worse. This may contribute to understand the often contradictoryevidence on the effect of professionalism.

3. Many „determinants“ of sophisticated behavior have only eclectic impact(e.g. wealth), only few seem to be of more systematic influence, such as experience.

Outline

Steps of analysis

1. Motivation and main findings

2. Data: compilation and participants

3. Descriptive information about investors‘ behavior

4. Regression analyses

5. Economic significance and robsutness

6. Conclusion

Data compilation

• Data come from an online survey of German investors conducted from 4. to 11. Nov. 2004 in cooperation with „sentix“.

• Sentix is a large online platform where registered investors reveal theirexpectations on financial and economic indicators and asset prices on a weekly basis.

• Rewards: users can view results and analyses provided

• Overall 497 responses (similar to the number of participants at that time- 75 institutional investors- 78 investmnet advisors- 344 individual investors (laymen)

Data quality: pretest, anonymous survey, no influence of single participants dueto large number (strategic distortion), intrinsic motivation is expected(interested in financial affairs, registered users, small reward)

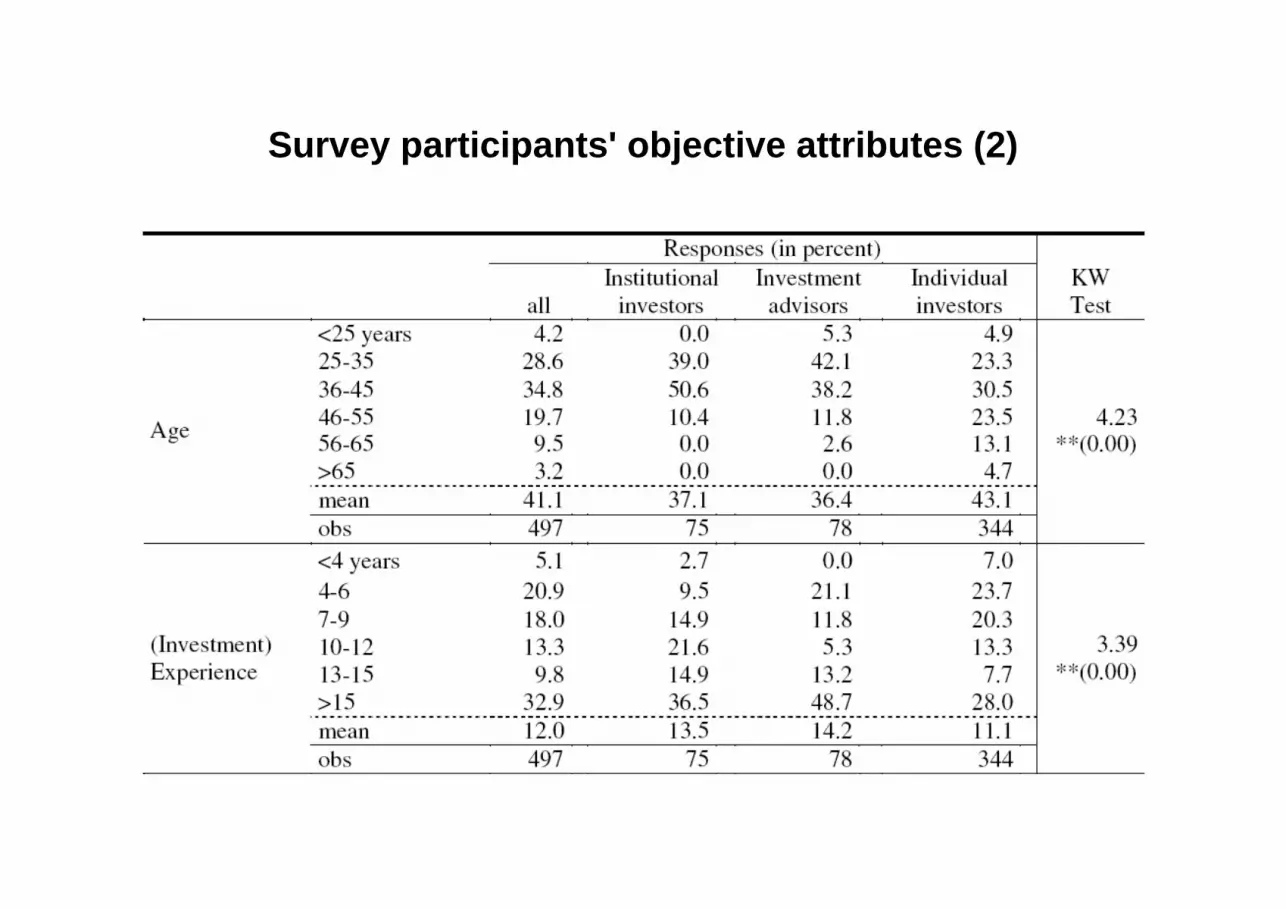

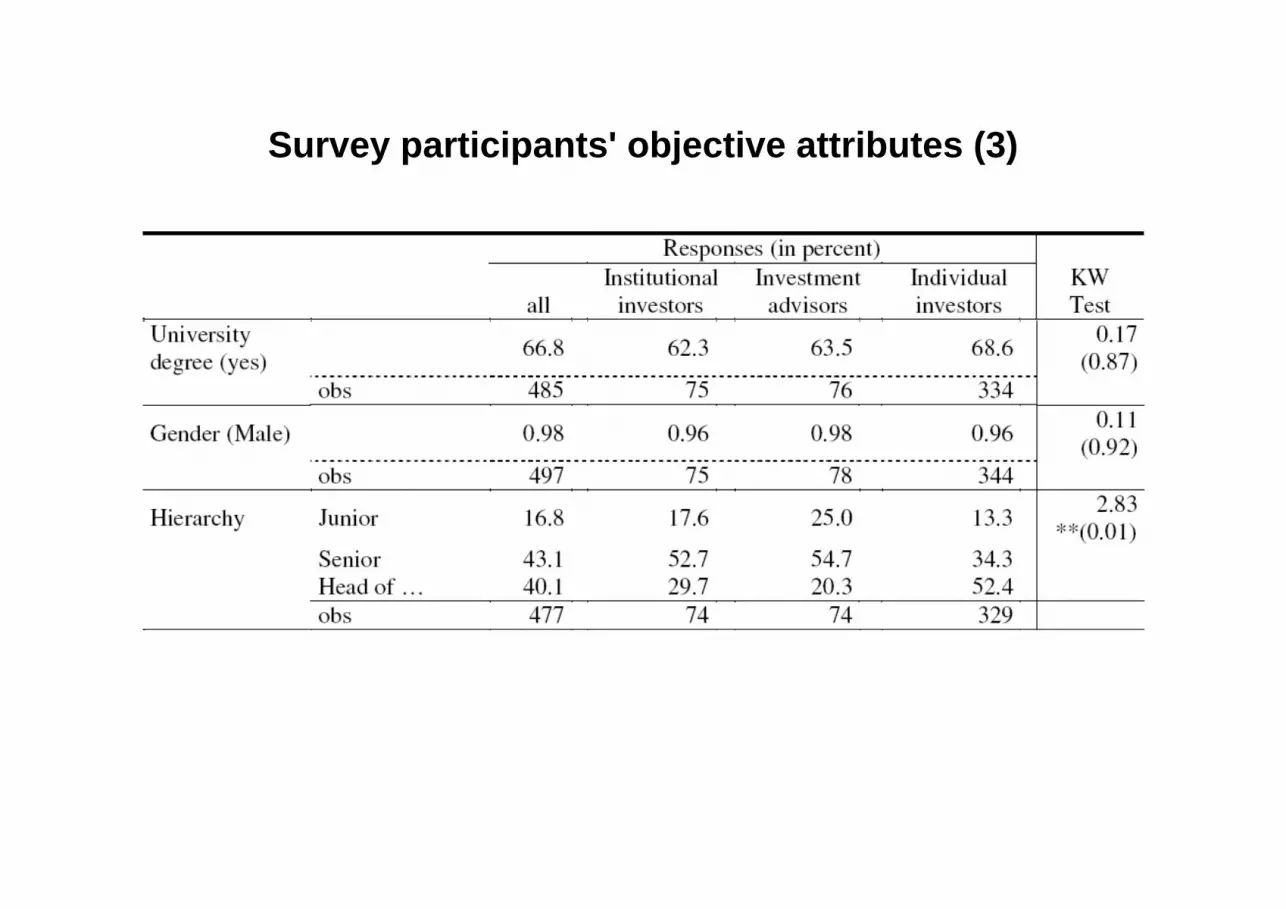

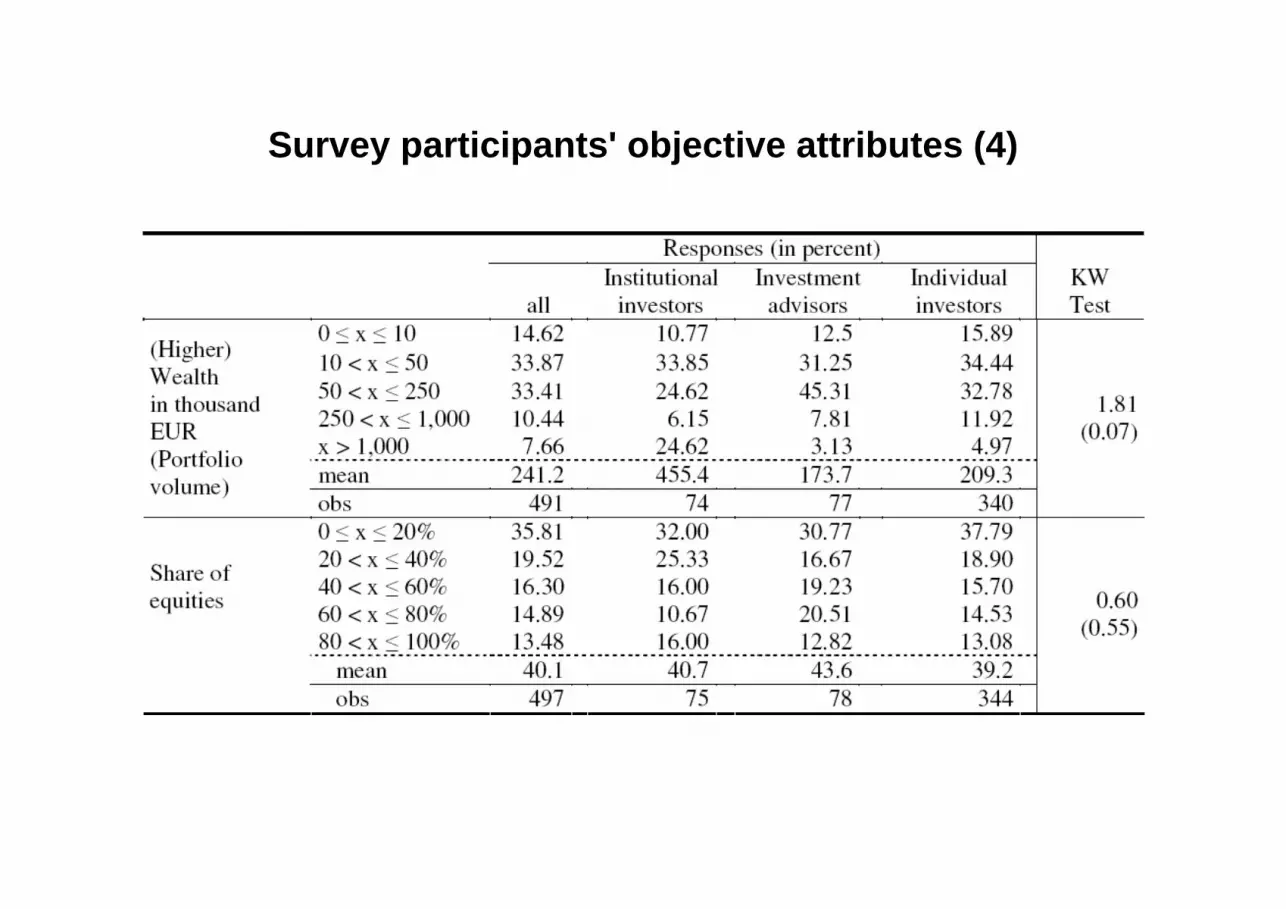

Participants‘ objective attributes (1)

1. The average investor of the survey is: 40 years old, 12 years investmnetexperience, university degree, male, senior position, about 250 tsd. europrivate securities, 40% equity share

2. Compared to other surveys or statistics: institutional investors are„normal“, individual are similar to other online broker investors but not to the normal population clearly no average investor

3. Investors groups differ in some characteristics to a statistically significantdegree:- indiv. investors are older, shorter experience, most senior positions- investment advisors relative to instit. inv.: shorter or longer experience- institutional investors: most wealthyThe sample is largely representative for institutional investors but toohighly qualified for individual investors heightens the stakes to find an effect from professionalism

Survey participants' objective attributes (2)

Survey participants' objective attributes (3)

Survey participants' objective attributes (4)

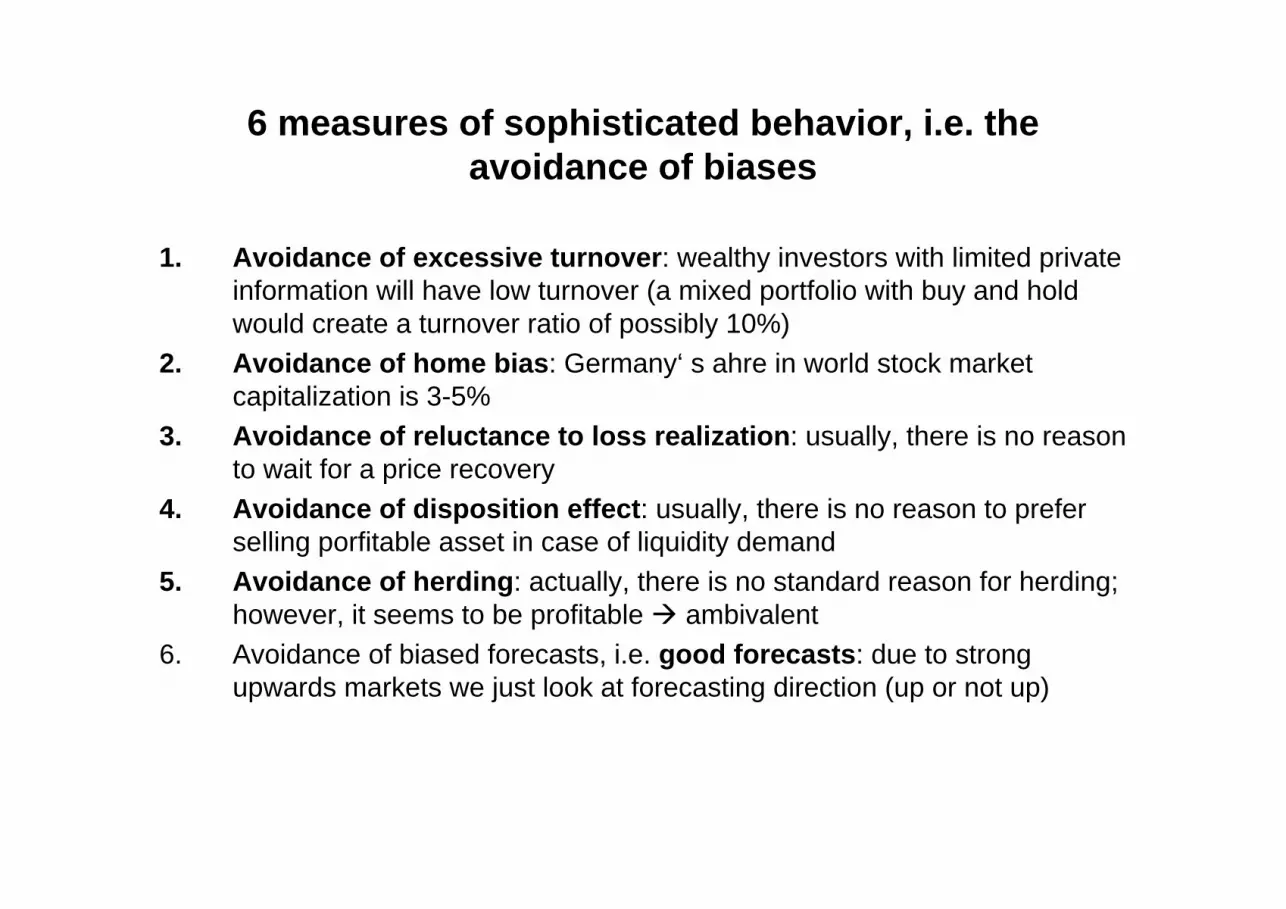

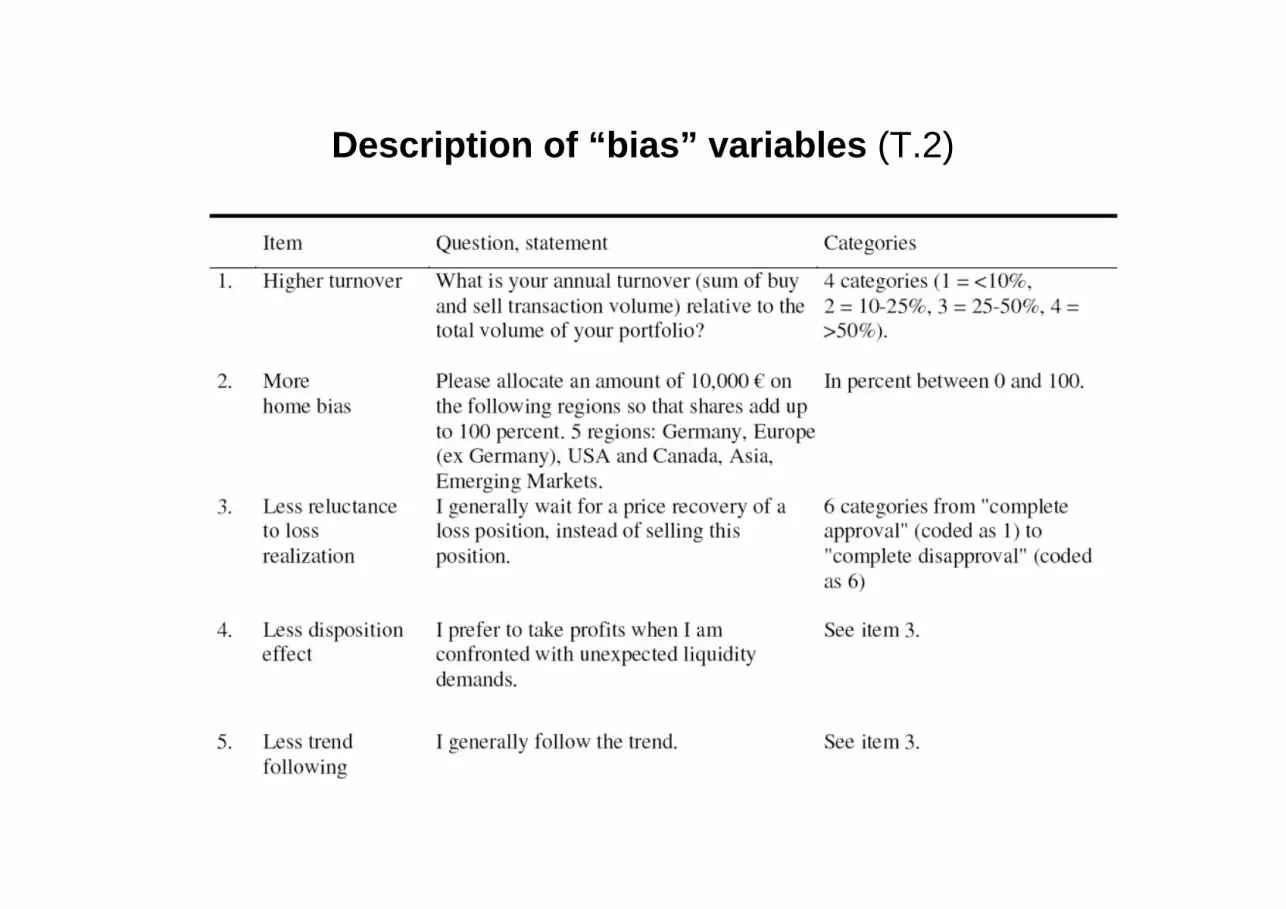

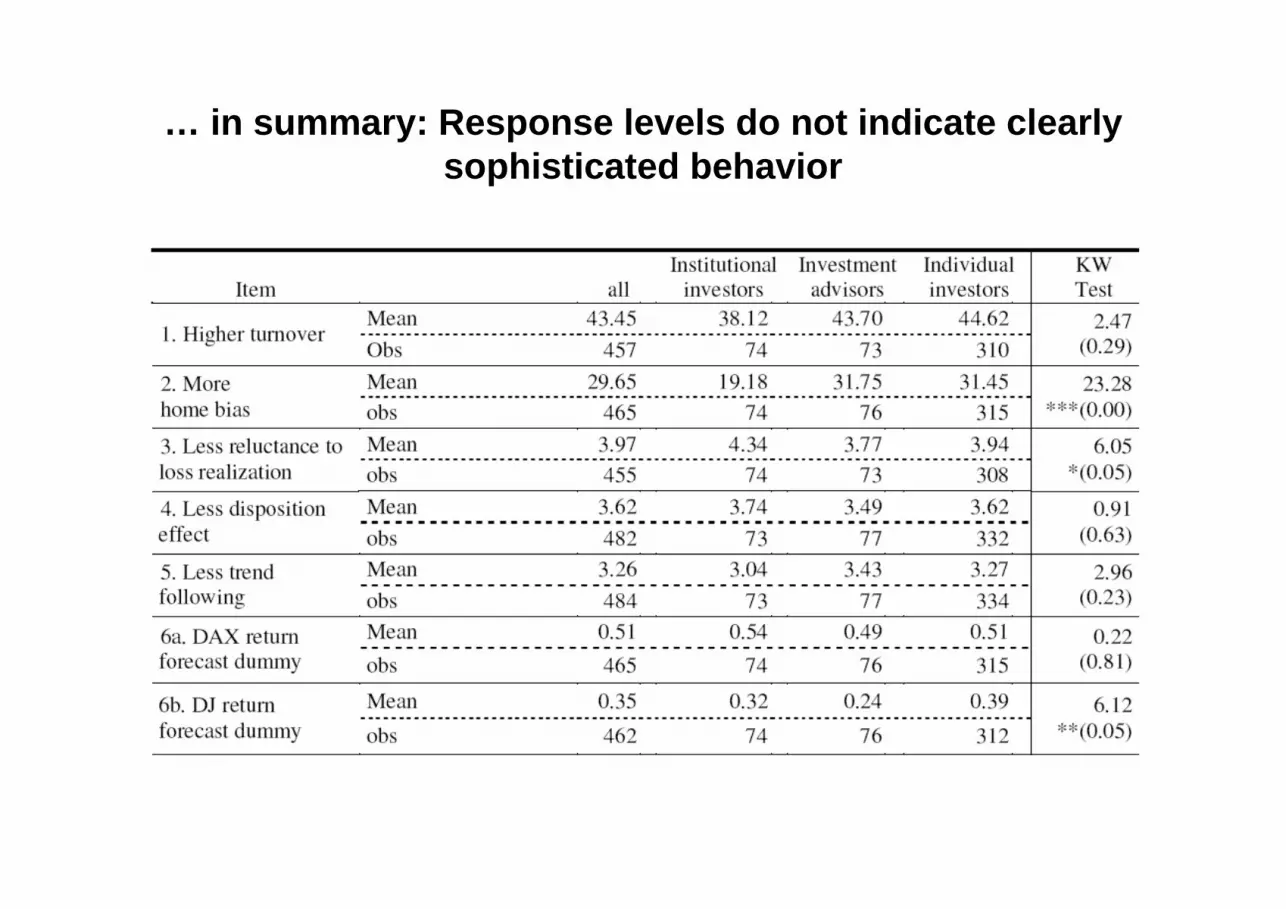

6 measures of sophisticated behavior, i.e. theavoidance of biases

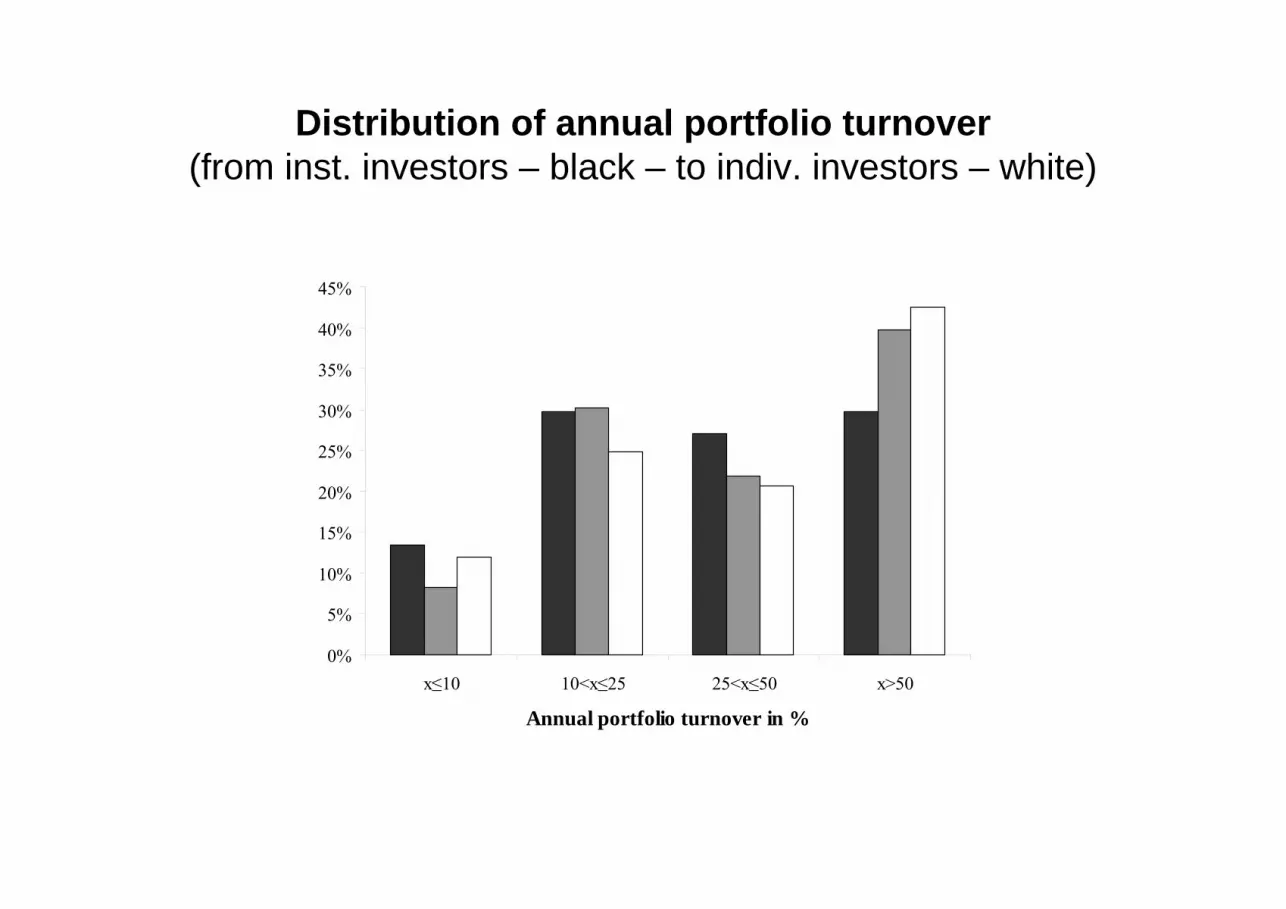

1. Avoidance of excessive turnover: wealthy investors with limited private information will have low turnover (a mixed portfolio with buy and hold would create a turnover ratio of possibly 10%)

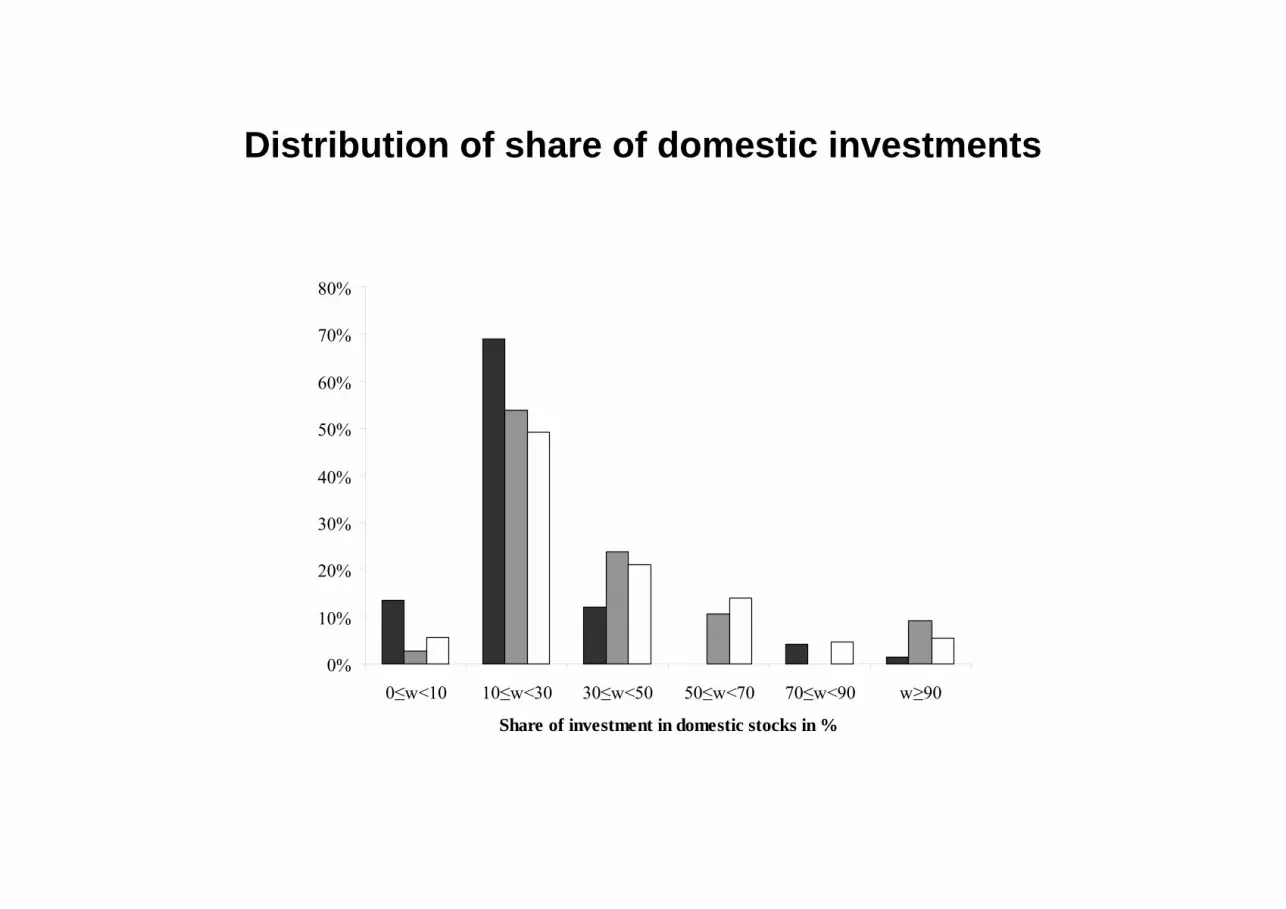

2. Avoidance of home bias: Germany‘ s ahre in world stock marketcapitalization is 3-5%

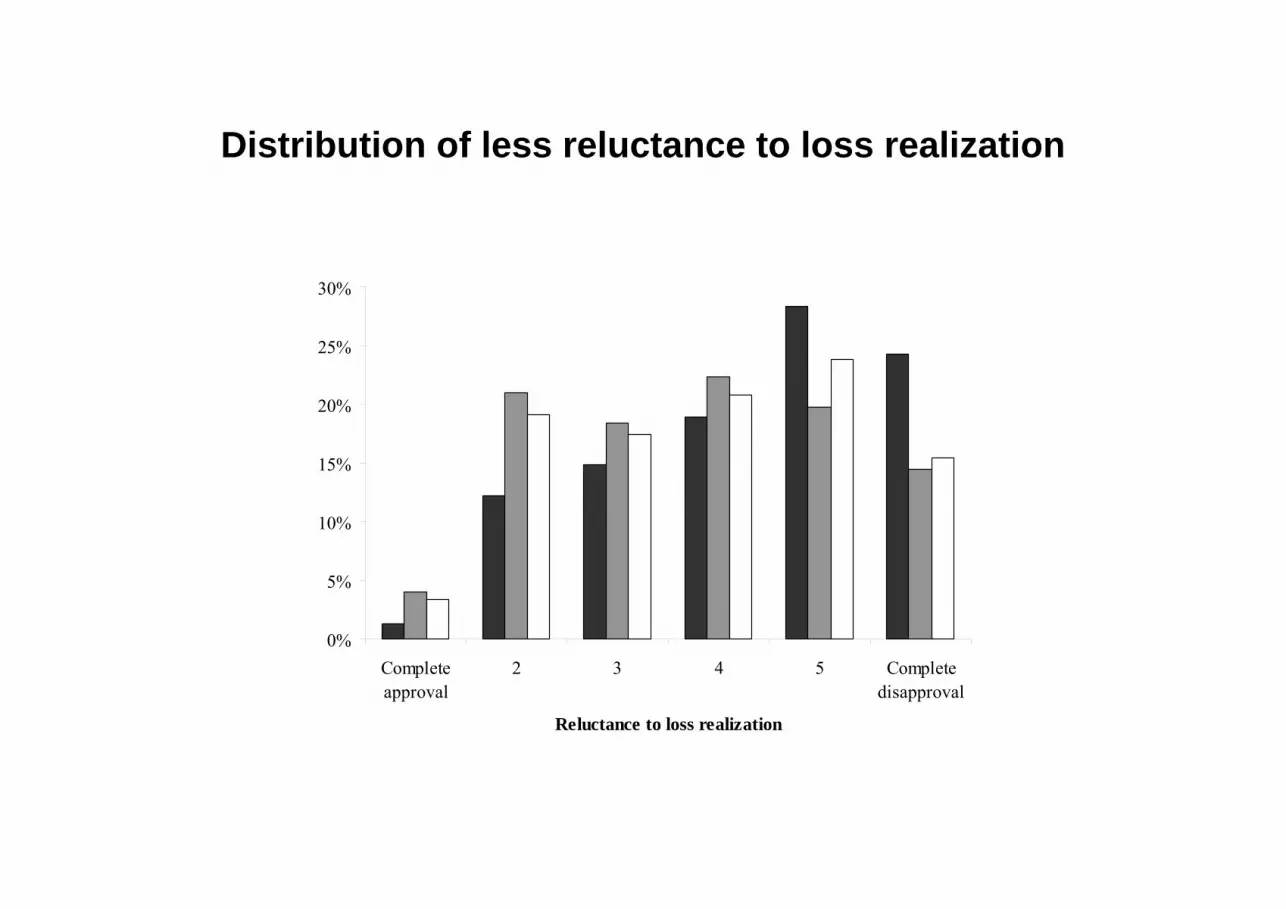

3. Avoidance of reluctance to loss realization: usually, there is no reasonto wait for a price recovery

4. Avoidance of disposition effect: usually, there is no reason to preferselling porfitable asset in case of liquidity demand

5. Avoidance of herding: actually, there is no standard reason for herding; however, it seems to be profitable ambivalent

6. Avoidance of biased forecasts, i.e. good forecasts: due to strongupwards markets we just look at forecasting direction (up or not up)

Description of “bias” variables (T.2)

Distribution of annual portfolio turnover(from inst. investors – black – to indiv. investors – white)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

x≤10 10<x≤25 25<x≤50 x>50

Annual portfolio turnover in %

Distribution of share of domestic investments

0%

10%

20%

30%

40%

50%

60%

70%

80%

0≤w<10 10≤w<30 30≤w<50 50≤w<70 70≤w<90 w≥90

Share of investment in domestic stocks in %

Distribution of less reluctance to loss realization

0%

5%

10%

15%

20%

25%

30%

Completeapproval

2 3 4 5 Completedisapproval

Reluctance to loss realization

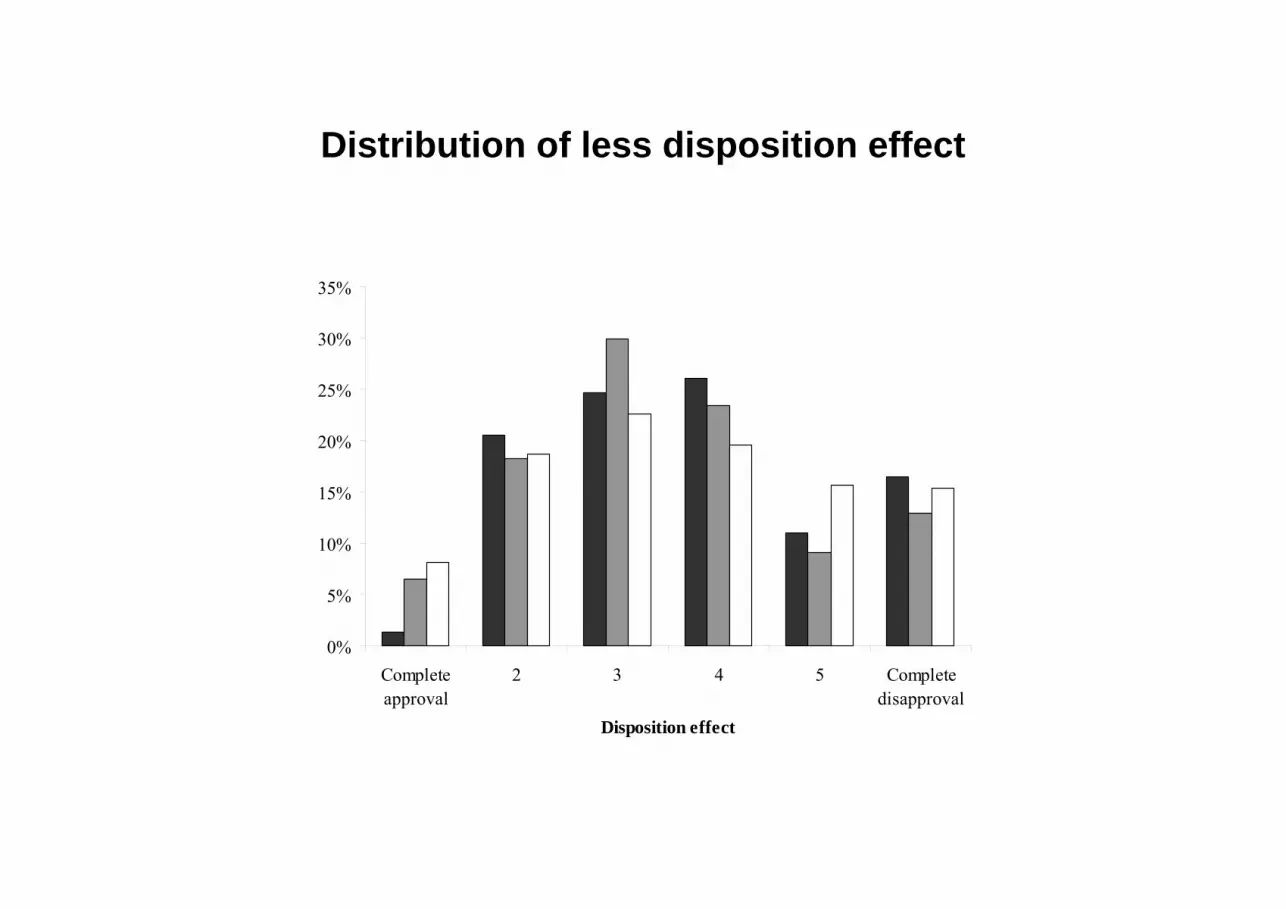

Distribution of less disposition effect

0%

5%

10%

15%

20%

25%

30%

35%

Completeapproval

2 3 4 5 Completedisapproval

Disposition effect

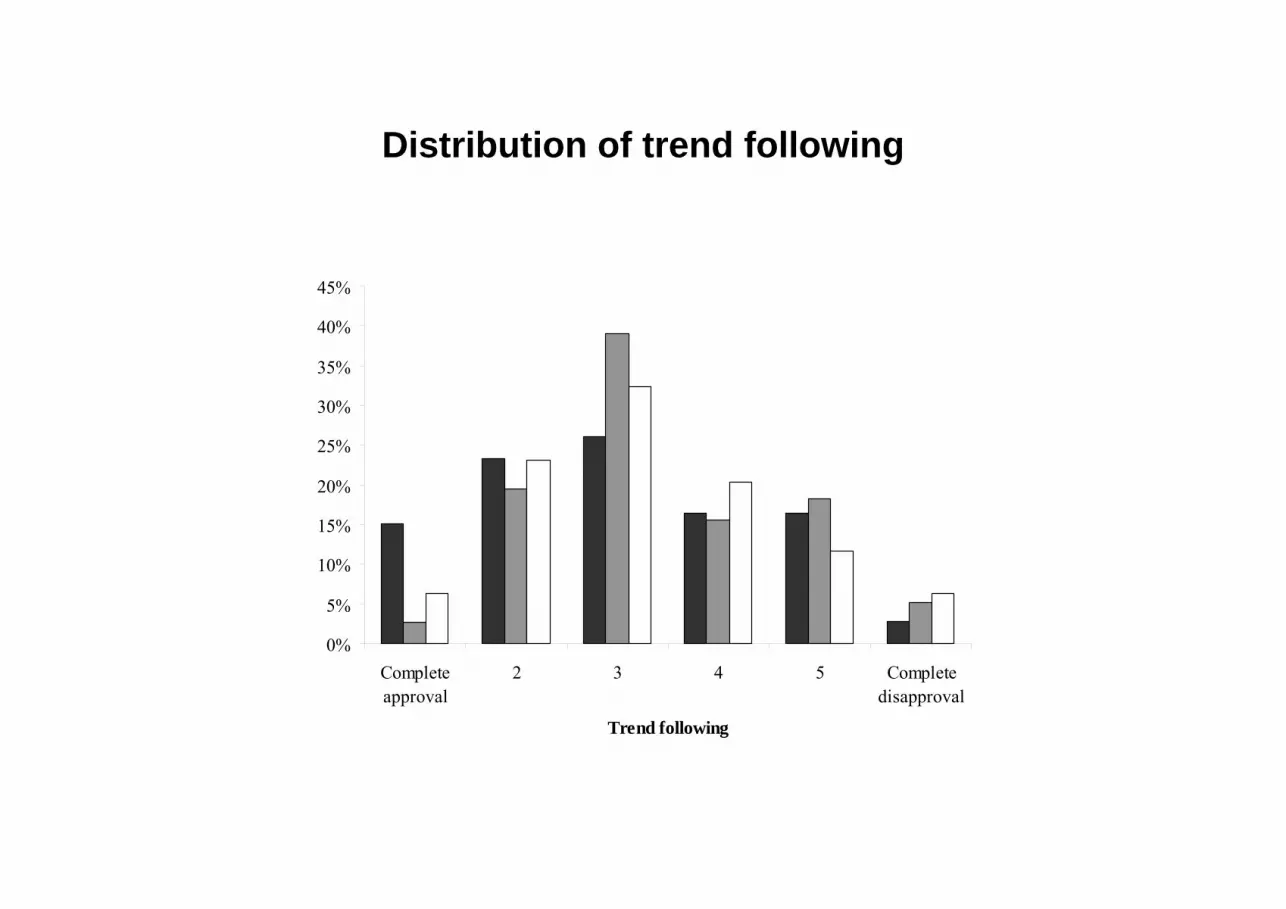

Distribution of trend following

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Completeapproval

2 3 4 5 Completedisapproval

Trend following

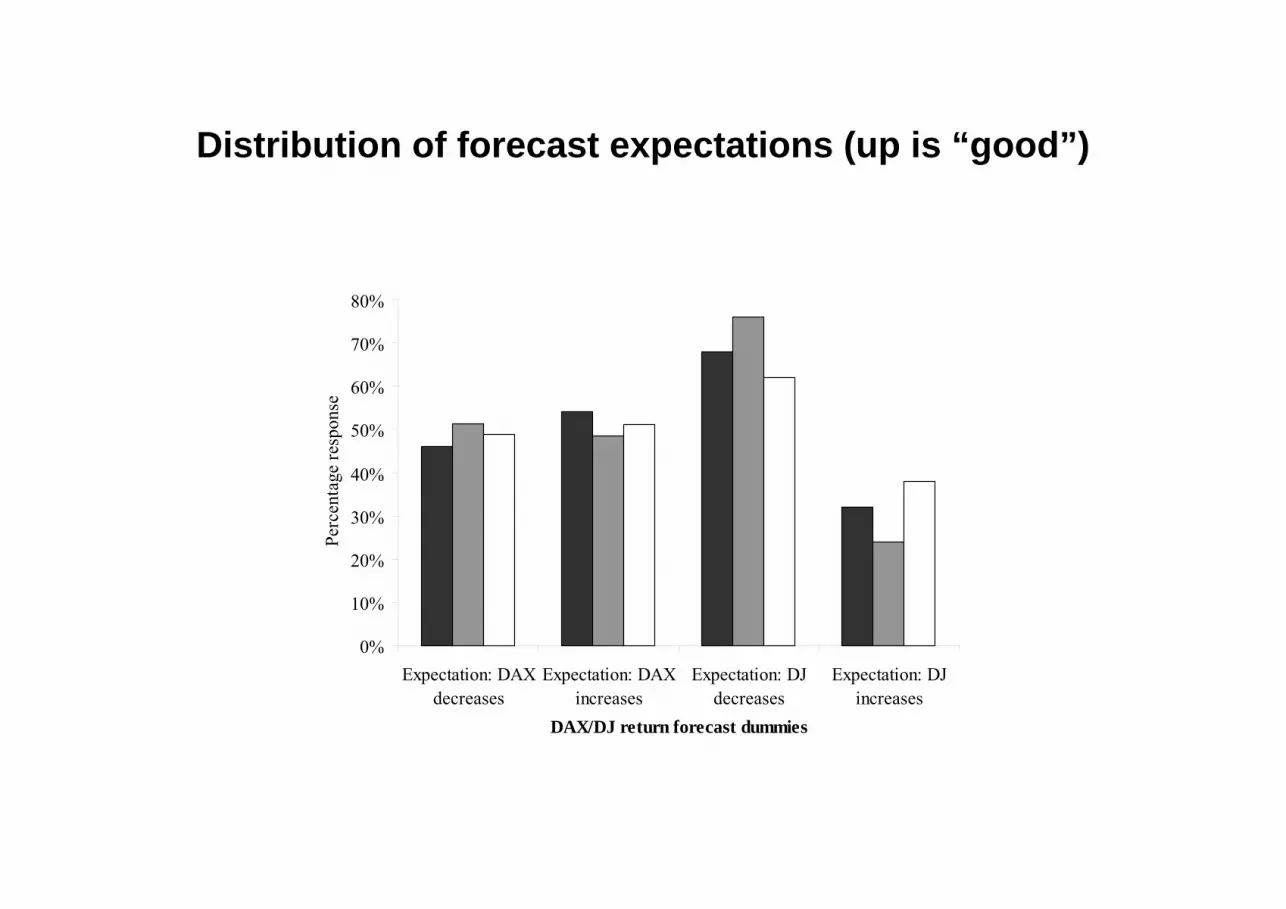

Distribution of forecast expectations (up is “good”)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Expectation: DAXdecreases

Expectation: DAXincreases

Expectation: DJdecreases

Expectation: DJincreases

DAX/DJ return forecast dummies

Perc

enta

ge re

spon

se

… in summary: Response levels do not indicate clearly sophisticated behavior

Consideration of further control variables

Investment behavior may be influenced by further investor attitudes

• General relevance: attitude towards risk aversion• General relevance: long-term forecasting horizon

• Home bias: local information advantage• Home bias: return optimism (regarding domestic investments)

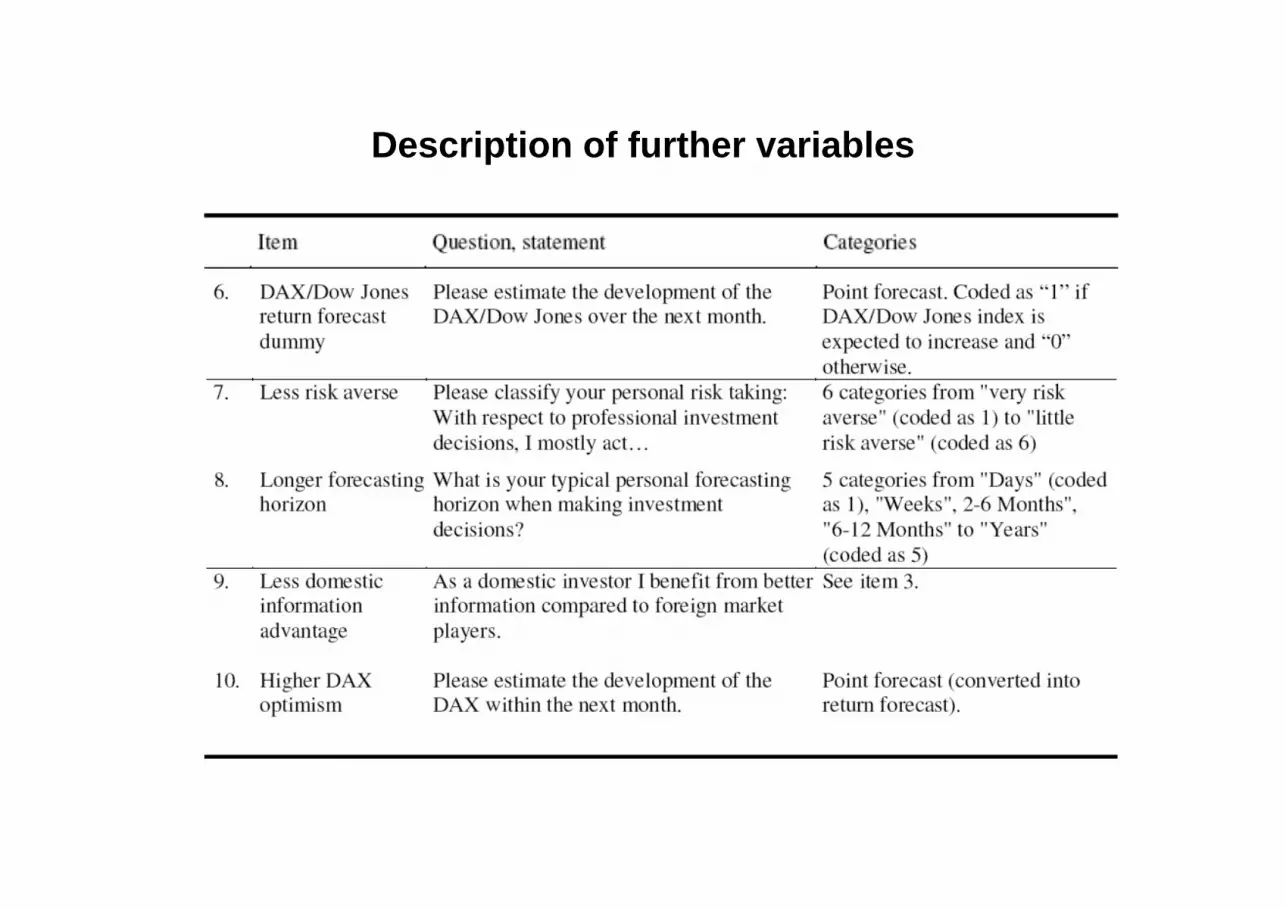

Description of further variables

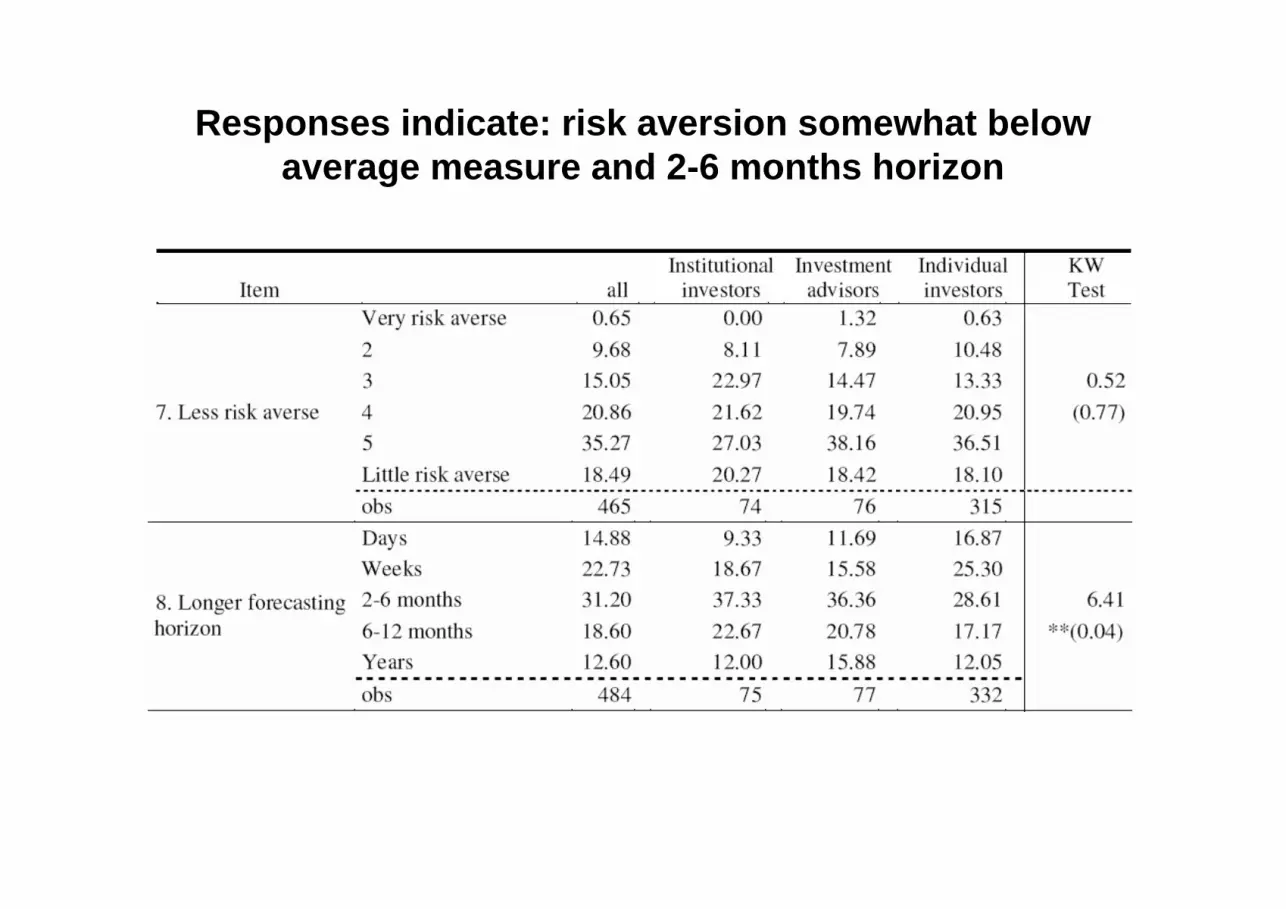

Responses indicate: risk aversion somewhat below average measure and 2-6 months horizon

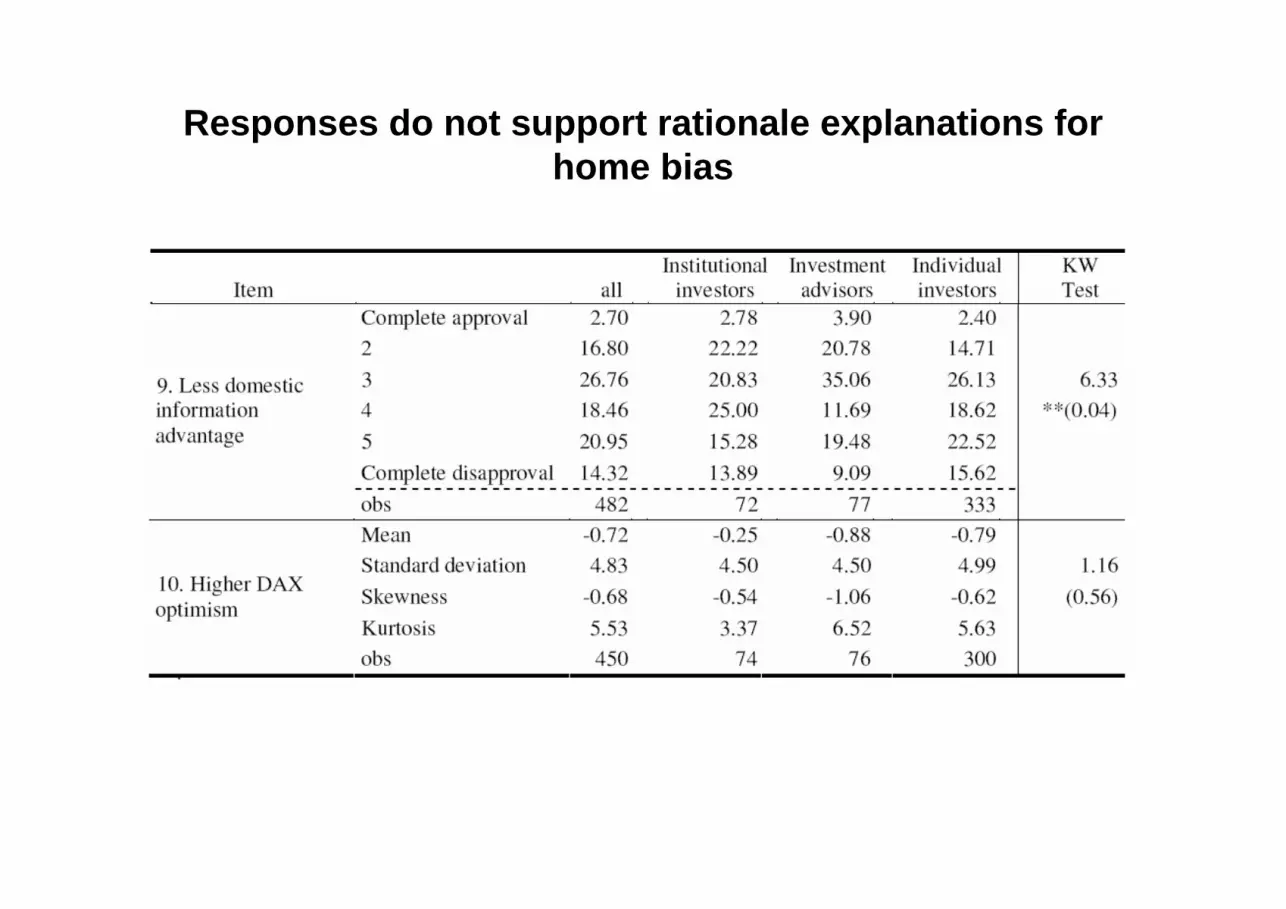

Responses do not support rationale explanations for home bias

4. Regression analyses: methods

• In most cases we employ ordered probit regressions (applies to 4 measuresof sophisticated behavior with 4 – 6 ordered response categories)

• In case of home bias we get percentage shares so we employ a censoredlinear regression (with censoring at 0 and 100 percent). For robustnesspruposes we also run an ordered probit where domestic investment iscaptured in 6 categories)

• In the cases of directional forecasting we rely on a simple bivariate probitregression.

Explanatory (RHS) variables in these regressions are in fact „correlates“.

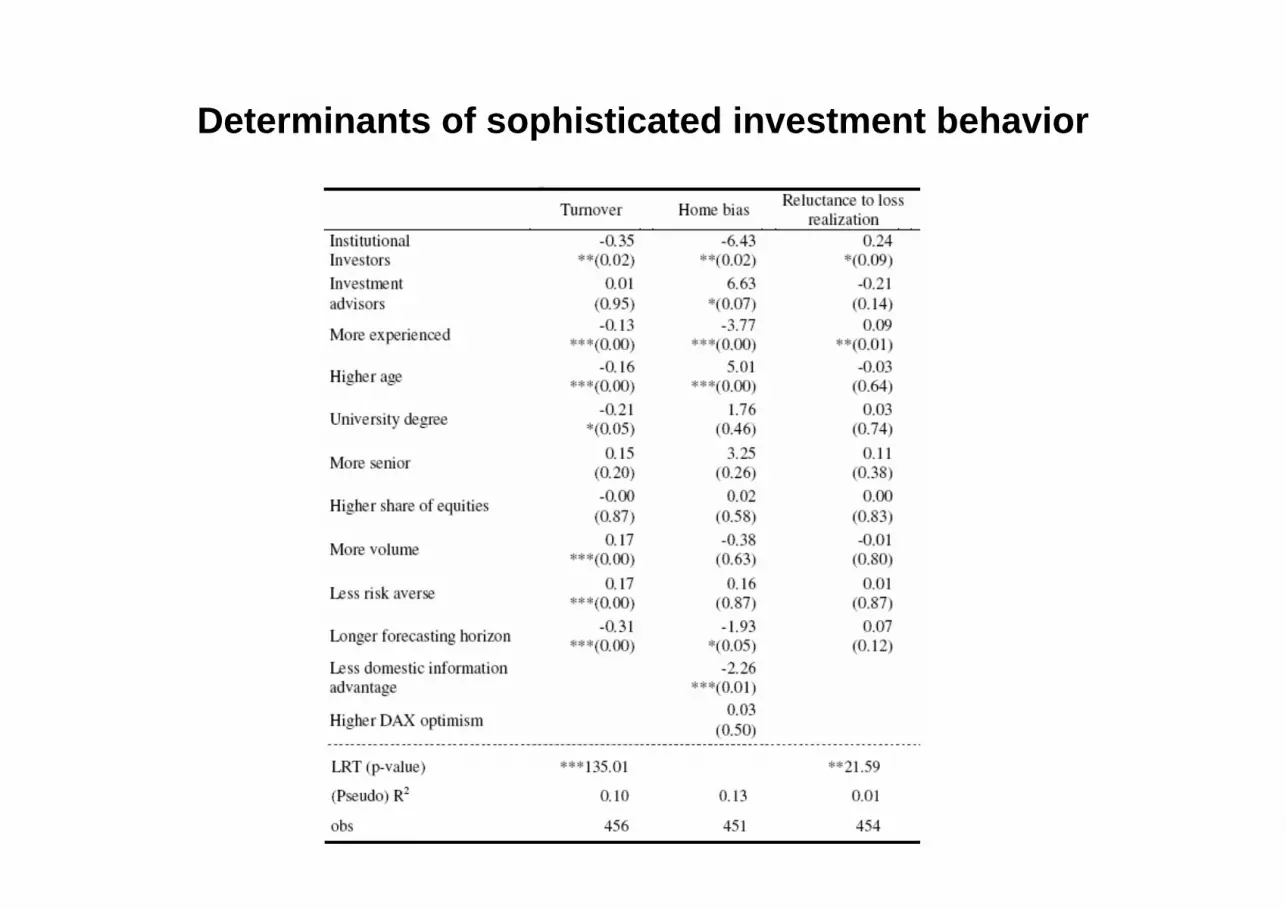

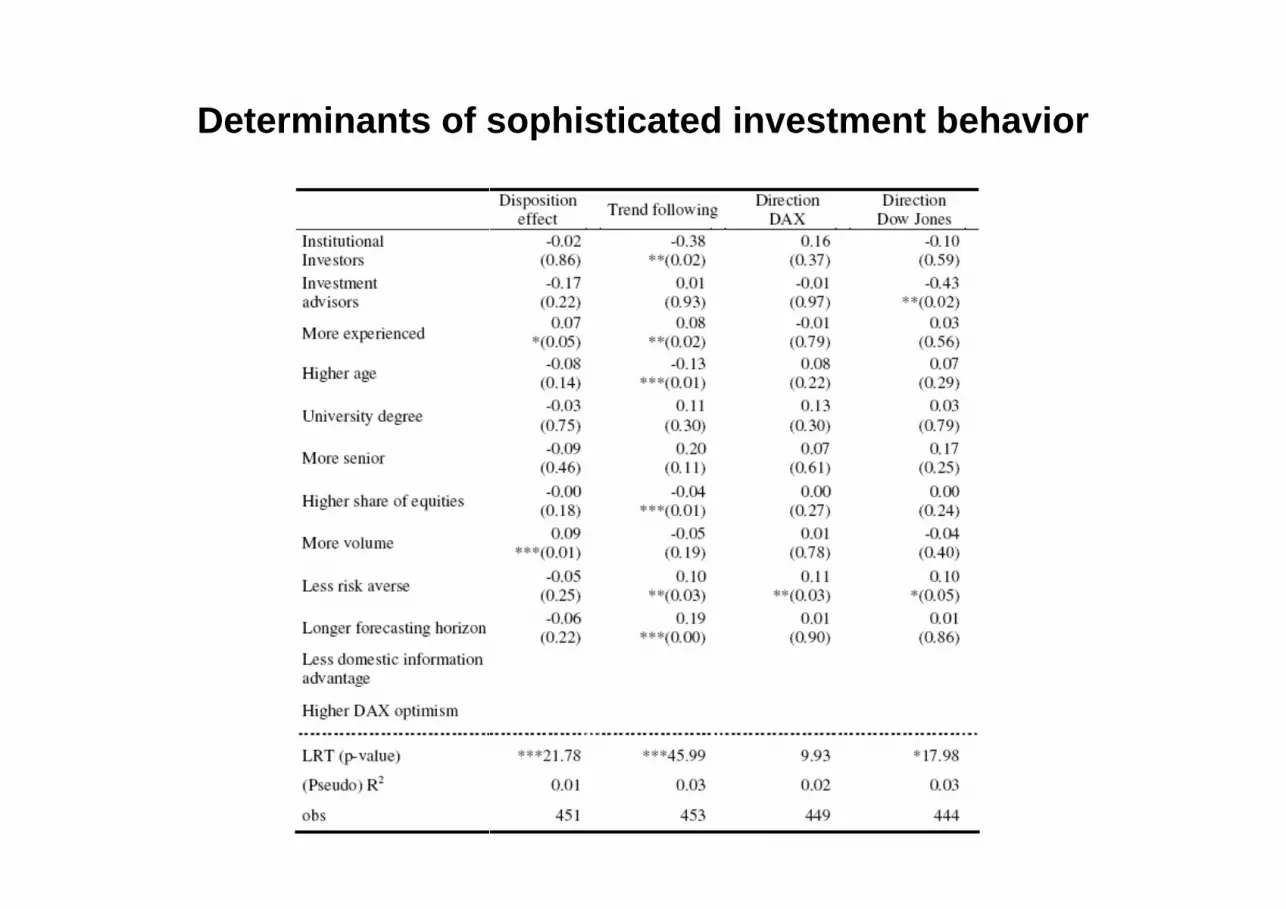

Determinants of sophisticated investment behavior

Determinants of sophisticated investment behavior

… summarizing: institutional investors show moresophisticated behavior, investment advisors do not

Results presented are in relation to the largest group, i.e. individual investors:

• Institutional investors show significantly less portfolio churning, less homebias, less reluctance to loss realization;they show more trend following, have the best DAX forecasts but areintermediate on less disposition effect and DJ forecasts

• Investment advisors show never sophisticated behavior but havesignificantly more home bias and make significantly the worst DJ forecasts.

• Thus, advanced individual investors are similar to some professionals, i.e. here investment advisors.

• Experience seems helpful for avoiding biases. Other variables only aresometimes important.

We conduct 3 further analyses

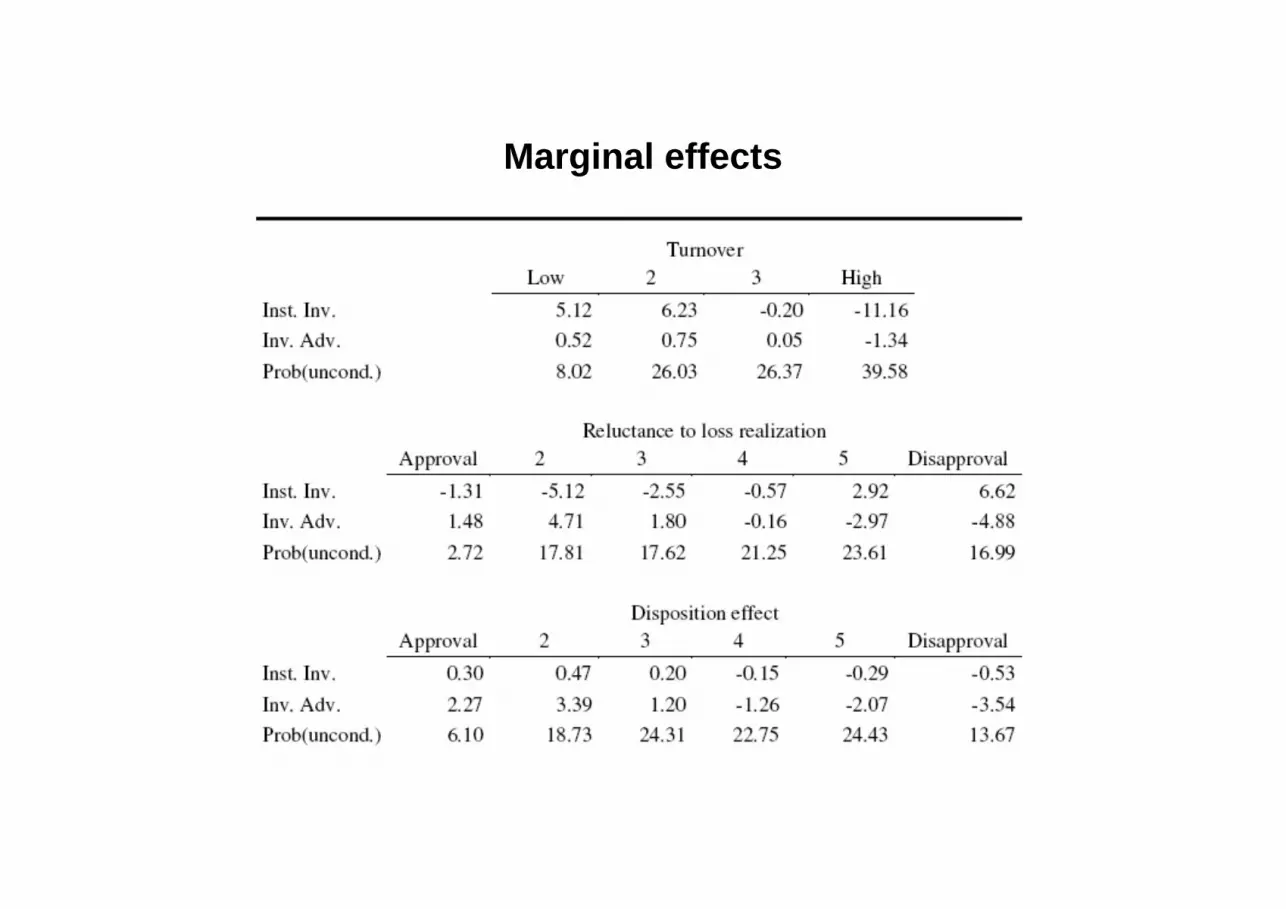

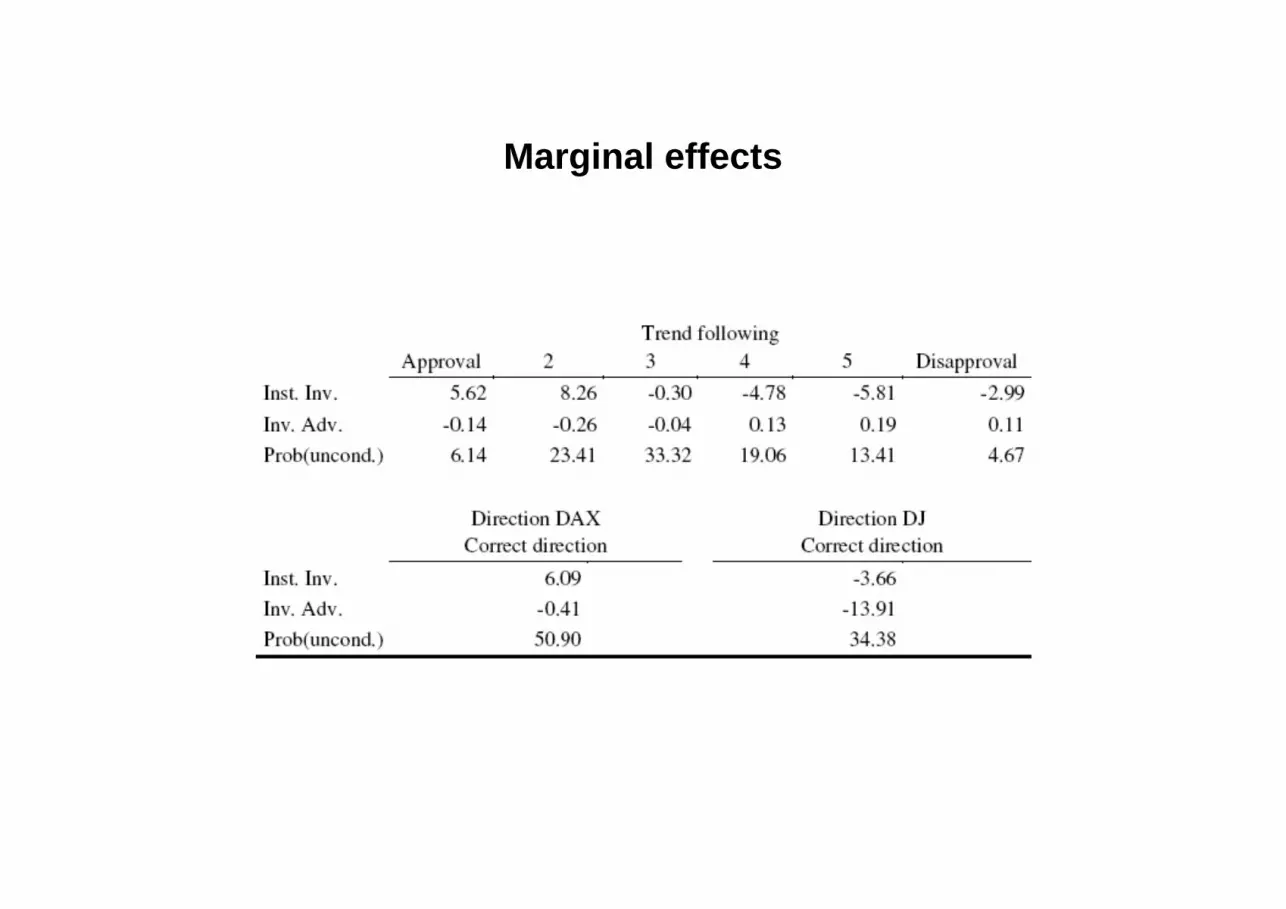

• Economic relevance (different from statistical significance): marginal effects of the two professionalism dummies in the ordered probite.g.: being an institutional investor increases the probability of being in oneof the 2 lower turnover categories form the unconditional probability of 34% by more than 11 percentage points to 45% the marginal effect is aboutone third of the unconditional probability.

• The differentiation between 2 groups of professionals: if we put theminto one group, there is no significant difference in behavior againstindoividual investors anymore. professionalism as such does not driveresults

• Robustness of specification: stepwise exclusion of insignificant variables does not change findings qualitatively.

Conclusions

• Research issue: professionals do not always behave (more) sophisticated (than laymen).

• We provide a new approach complementing available evidence: survey with 4 highlights (comprehensiveness regarding biases, 3 groups of investors, controls, less interference)

Findings: 1. Also professional investors are subject to some degree of biased

investment behavior

2. Professionals are not alike: Institutional investors behave moresophisticated than laymen whereas investment advisors seem to berather worse. This may contribute to understand the often contradictoryevidence on the effect of professionalism.

3. Many „determinants“ of sophisticated behavior have only eclectic impact(e.g. wealth), only few seem to be of more systematic influence, such as experience.

Thank you for your attention!

Marginal effects

Marginal effects