Model Test Paper - 1 IPCC Gr. II Paper - 6 Auditing and Assurance Question No. 1 is compulsory. 1. Discuss the following: (a) Standards collectively known as the Engagements Standards issued by AASB under the authority of the council of ICAI. (5 marks) Answer: The following standards issued by the Auditing and Assurance Standards Board under the authority of the Council are collectively known as the Engagement Standards. 1. Standards on Auditing (SAs): To be applied in the audit of historical financial information . 2. Standards on Review Engagements (SREs): To be applied in the review of historical financial information. 3. Standards on Assurance Engagements (SAEs): To be applied in assurance engagements, dealing with subject matters other than historical financial information. 4. Standards on Related Services (SRSs): To be applied to engagements involving application of agreed-upon procedures to information, compilation engagements, and other related services engagements, as may be specified by the ICAI. (b) Is surprised checks desirable in audit, if so give important recommendations. (5 marks) Answer: 1. One of the most important parts of audit is the surprise check, the results of these checks are very helpful to the auditor as they help in deciding the scope of audit and also the reports. 2. Effectiveness of the audit is improved by the element of surprise. This element is also incorporated in audit programmes. 3. The element of surprise in an audit may be both in relation to the time of audit, that is selection of date, when the auditor will visit the clients office for audit and selection of the areas of audit. 6.1

Transcript

Model Test Paper - 1IPCC Gr. IIPaper - 6

Auditing and AssuranceQuestion No. 1 is compulsory.

1. Discuss the following:(a) Standards collectively known as the Engagements Standards issued

by AASB under the authority of the council of ICAI. (5 marks)Answer:The following standards issued by the Auditing and AssuranceStandards Board under the authority of the Council arecollectively known as the Engagement Standards.1. Standards on Auditing (SAs): To be applied in the audit of

historical financial information .2. Standards on Review Engagements (SREs): To be applied in

the review of historical financial information.3. Standards on Assurance Engagements (SAEs): To be

applied in assurance engagements, dealing with subject mattersother than historical financial information.

4. Standards on Related Services (SRSs): To be applied toengagements involving application of agreed-upon proceduresto information, compilation engagements, and other relatedservices engagements, as may be specified by the ICAI.

(b) Is surprised checks desirable in audit, if so give importantrecommendations. (5 marks)Answer:1. One of the most important parts of audit is the surprise check,

the results of these checks are very helpful to the auditor asthey help in deciding the scope of audit and also the reports.

2. Effectiveness of the audit is improved by the element ofsurprise. This element is also incorporated in audit programmes.

3. The element of surprise in an audit may be both in relation tothe time of audit, that is selection of date, when the auditor willvisit the clients office for audit and selection of the areas ofaudit.

6.1

6.2 O Solved Scanner IPCC Group- II Paper - 6

4. Auditor’s visits for a surprise check in order to know whether theinternal control system is working effectively or not and whetherall accounting and other records are kept up to the date as perthe statutory regulation.

5. These checks and surprise visits can bring good moral check onthe client’s staff.

6. Surprise checks also help in determining the errors and frauds.7. Surprise checks are very helpful for the organization having

weak internal control system, very large and diversified.8. Extent of the check will depend upon the auditor.9. The consequences of the surprise check should be

communicated to the management. This is done to overcomethe weakness.

10. The auditor gets satisfied only when proper actions are taken bythe management on the matters communicated by him.

(c) Filling of a casual vacancy of auditor in respect of a company audit.(5 marks)

Answer:Filling of a Casual VacancyAs per Sec. 139(8) of Companies Act, 2013, any casual vacancyin the office of an auditor shall:(i) In the case of a company other than a company whose

accounts are subject to audit by an auditor appointed bythe Comptroller and Auditor-General of India, be filled by theBoard of Directors within thirty days.If such casual vacancy is as a result of the resignation of anauditor, such appointment shall also be approved by thecompany at a general meeting convened within three months ofthe recommendation of the Board and he shall hold the office tillthe conclusion of the next annual general meeting;

(ii) In the case of a company whose accounts are subject toaudit by an auditor appointed by the Comptroller andAuditor-General of India, be filled by the Comptroller andAuditor-General of India within thirty days:

Model Test Paper O 6.3

In case the Comptroller and Auditor-General of India does notfill the vacancy within the said period the Board of Directors shallfill the vacancy within next thirty days.

(d) Director's responsibility statement. (5 marks)Answer:As per Sec. 134(3)(c) of Companies Act, 2013, the report of Boardof Directors on annual accounts shall also include a ‘Directors’Responsibility statement.As per Sec. 134(5), the Directors’ Responsibility Statement shallstate:1. in the preparation of the annual accounts, the applicable

accounting standards had been followed along with properexplanation relating to material departures;

2. the directors had selected such accounting policies and appliedthem consistently and made judgments and estimates that arereasonable and prudent so as to give a true and fair view of thestate of affairs of the company at the end of the financial yearand of the profit and loss of the company for that period;

3. the directors had taken proper and sufficient care for themaintenance of adequate accounting records in accordancewith the provisions of this Act for safeguarding the assets of thecompany and for preventing and detecting fraud and otherirregularities;

4. the directors had prepared the annual accounts on a goingconcern basis; and

5. the directors, in the case of a listed company, had laid downinternal financial controls to be followed by the company andthat such internal financial controls are adequate and wereoperating effectively.Explanation: For the purposes of this clause, the term “internalfinancial controls” means the policies and procedures adoptedby the company for ensuring the orderly and efficient conduct ofits business, including adherence to company’s policies, thesafeguarding of its assets, the prevention and detection of

6.4 O Solved Scanner IPCC Group- II Paper - 6

frauds and errors, the accuracy and completeness of theaccounting records, and the timely preparation of reliablefinancial information; and

6. the directors had devised proper systems to ensure compliancewith the provisions of all applicable laws and that such systemswere adequate and operating effectively.

2. State with reason. (Answer any eight)(i) SA - 402 deals with responsibility of the auditor of the service

organisation. (2 marks)Answer:False : SA 402, Audit Considerations Relating to an Entity Usinga Service Organisation, establishes standards for the auditors of anentity (i.e. client) that uses a service organisation. AAS-24 thus,does not deals with responsibility of the auditor of the serviceorganisation.

(ii) Confirmations received by the auditor directly from third parties areconclusive evidence in support of a transaction. (2 marks)Answer:False: Confirmations received directly from the third parties by theauditor are more reliable but same cannot be treated as conclusiveevidence.

(iii) Auditing in depth implies that the auditor vouches almost alltransactions in a manner that the chances of not checking anytransaction are left at minimum. (2 marks)Answer:False : Auditing in depth does not mean the 100% vouching. It ischecking selected transactions from beginning to end to understandthe entire system within which the transaction passes through.

(iv) For the purpose of SA - 600 “Principal Auditor” means the partner ofthe firm signing the Audit report. (2 marks)

Model Test Paper O 6.5

Answer:False : As per SA 600, Using the Work of Another Auditor,“Principal Auditor” means the auditor with responsibility for reportingon the financial information of an entity when that financialinformation includes the financial information of one or morecomponents audited by another auditor. Therefore, it is not correctto say that for the purpose of SA 600 “Principal Auditor” meansthe partner of the firm singing the Audit report.

(v) There is direct relationship between detection risk and combinedlevel of inherent and control risk. (2 marks)Answer:False : There is an inverse relationship between detection risk andcombined level of inherent risk and control risk, because if inherentand control risk decreases detection risk increases.

(vi) The first auditor of a Government company was appointed by theBoard in its meeting after 10 days from the date of registration.

(2 marks)Answer:Incorrect: As per Sec. 139(7), the appointment of first auditor of a

government company shall be done by Comptroller and AuditorGeneral of India (CAG) within 60 days from the date ofregistration of the company.

(vii) The Auditor shall express an unqualified opinion if the Auditor isunable to obtain sufficient audit evidence regarding the openingbalances. (2 marks)Answer:This statement is incorrect. When auditor is unable to obtainsufficient audit evidence regarding the opening balances he shallexpress a qualified opinion.

(viii) Internal auditor of the company cannot also be its cost auditor.(2 marks)

6.6 O Solved Scanner IPCC Group- II Paper - 6

Answer:True : Internal auditor cannot be appointed as cost auditor. As perrule 14 of the Companies (Audit and Auditors) Rules, 2014, in caseof companies which are required to constitute an audit committeethe Board shall appoint a cost auditor who is a cost accountant inpractice or a firm of cost accountants in practice on recommendationof audit committee.

(ix) Taking management representation is a convenient, economical andequally acceptable auditing method even where the direct access byauditor to audit evidence is possible. (2 marks)Answer:False : If it is possible for auditor to check the transaction by himselfthrough direct access, it is not fair for him to merely rely themanagement representation as prime audit evidence.

(x) An expert for the purpose of SA - 620 is a person, firm or associationof persons possessing special skill, knowledge and experience inauditing. (2 marks)Answer:False : It has been clearly mentioned in SA 620 Using the work ofan Auditor’s Expert, an expert, (or a specialist), for the purpose ofthis statement, is a person, firm or other association of personpossessing special skill, knowledge and experience in a particularfield other than accounting and auditing.

3. How will you vouch/verify the following:(a) Payment for Acquisition of Assets (4 marks)

Answer :Payment for Acquisition of Assets:The asset if acquired for the business, then payment made shall bein the capital nature expenditure and it should be included in thecost of fixed assets of the company. Such payment shall be eitheron the agreed term or quotation term or the market term. Such,payment shall be made in cash or through Bank.

Model Test Paper O 6.7

In this case, auditor should ensure that such payments are actuallymade and should also check the entry in seller books. He shouldalso check the amount and validity of the payment.

S.No.

Documents to bevouched

Aspects to be verified

1. Bill or Receipt The purchase of an asset must be dulysupported by the receipt for the amountpaid.

2. Title Deed in caseof Purchase ofImmovableProperty

In case of an immovable property theauditor must also inspect the title deeds.The title of an immovable property passesonly on registration. It is thereforeessential for an auditor to see thatproperty has been registered in thepurchaser’s name as required by therelevant regulations and also that the titleof the transfer to sell property has beenverified by a solicitor or an advocate.

3. RegistrationDocument incase of purchaseof movableproperty

In the case of movable property requiringregistration of ownership, e.g., a car or aship, it must be verified that such aregistration has been made in favour ofthe purchaser. It is necessary for theauditor to satisfy himself generally asregards existence, value and title of theassets acquired.

4. Authorisation ofPurchase byBoard

It must also be verified that the assetswere purchased only by a person whohad the authority to do so. CompaniesAct, 2013 provides that only the Board ofDirectors can invest the funds of thecompany. Thus the Board alone cansanction the purchase of a fixed asset.

6.8 O Solved Scanner IPCC Group- II Paper - 6

5. FinancialTreatment

• If the benefit of an item of expensehas been acquired by the purchaseralong with the asset, its value shouldbe debited to a separate account,e.g., when a motor car has beenpurchased on which certain taxes andinsurance charges were paid by theseller for a period that had notexpired.

• In the case of an asset constructed ormanufactured by the client himself,e.g., where a building has beenconstructed or a plant or machinerymanufactured by the concern with itslabour and materials, it must beverified that the cost of labour,materials and other direct expensesincurred has been charged as cost ofthe asset on a proper allocation of thetotal expenditure debited under theseheads.

• It must also be seen that neitherexpenses on repa i rs andmaintenance have been capitalisednor the cost of additions to assetscharged off as revenue expenses.

(b) Recovery of bad debts written off (4 marks)Answer:Recovery of Bad Debts written off can be verified as followsSl.No.

Document to bevouched

Aspects to be verified

1. Schedule of baddebts

Verify whether the amount of bad debtsrecovered has been shown in the baddebts schedule of the preceding years.

Model Test Paper O 6.9

2. Proof ofcollection

Verify the relevant proof of recoverysubmitted,e.g: Court/Tribunal decree, notice frombankruptcy trustee, letters fromcollecting agency or lawyer or party etc.

3. Credit manager'sfile

(i) Verify whether amount receivedhas been noted in the file.

(ii) Ascertain any specific mattermaterially affecting accounts hasbeen noted in the file.

4. Bank statement (i) Trace receipt of amount in Bankstatement

(ii) Confirm that the cheque receivedfrom party has not beendishonoured.

5. Receipt Verify whether proper acknowledgmentshave been issued to parties.

(c) Proposed dividend. (4 marks)Answer:Proposed dividend :1. Proposed dividend is to be provided for even though it is

proposed and is to be declared after the end of the accountingperiod in terms of AS 4 and also Schedule III disclosurerequirements.

2. The auditor should check the amount of paid up share capitaland verify the quantum of dividend proposed by checking thecalculations.

3. The auditor should check the minutes of the Board for theamount of dividend proposed to be considered for its declarationin general meeting.

4. Dividend tax payable on proposed dividend should be providedfor.

6.10 O Solved Scanner IPCC Group- II Paper - 6

5. The interim dividend if any paid should be checked andascertained that the proposed dividend is properly computed byadjustment to it, if the same had been reckoned for the totaldividend.

6. The account should be properly disclosed in statement of P&Laccount and also in Financial Statement according to therequirements of Schedule III to the Companies Act, 2013.

(d) Advances to suppliers. (4 marks)Answer:Advance given to Suppliers :Sl.No.

Document to bevouched

Aspects to be verified

1. Schedules andLedgers

Get the debit balance schedule in theaccount of creditors and giveparticular attention to the age of thebalances.Also examine in detail Bought Ledger.

2. AccountingTreatment

Investigate the unadjusted outstandingand check if any of them requireprovisioning.Also examine that according toSection 143(1)of the IndianCompanies Act, 2013, the advanceshave not been shown as deposits inthe B/S.

3. Final Documents Obtain the confirmation of balancesand ensure that any discrepancies ordifferences have been properlyreconciled.

4. (a) As an auditor of a Limited Company, you observe that during themonth of March, 2009, sales invoices were not recorded in books ofaccounts. You also observe that payment of wages was muchhigher compare to last year. Keeping in mind above, analysepossible ways of manipulation of accounts. (6 marks)

Model Test Paper O 6.11

Answer:Manipulation of Accounts : Accounts are falsified in order toconceal the true position of the business for some purpose. They arealways intentional, for a predetermined purpose and are generallycommitted either by the owners or top management personnel orsenior officers of the business. This type of fraud is generallycommitted:1. to avoid incidence of income-tax or other taxes by showing

profits at a lower figure.2. to withhold declaration of dividend even there is adequate profit.3. for receiving higher remuneration where managerial

remuneration is payable by reference to profits.4. for delaying a dividend when there are insufficient profits by

showing profits at inflated figures.Such types of frauds are difficult to be detected as they arecommitted by persons holding position of trust and use carefullyguarded by them. Such frauds are generally of the following nature:1. Recording fictitious purchases or suppression of purchases2. Recording fictitious sales or omission of sales3. Recording fictitious expenses or omission of expenses4. Over valuation or under valuation of stock.5. Taking credit for accrued income not likely to be received or

omission of income.6. Revenue expenses changed to capital and vice-versa. AAS 4

(new SA 240) “Auditor’s Responsibility to consider fraud andError in an Audit of Financial Statements” deals with theauditor’s responsibilities for the detection of materialmisstatement resulting from fraud and error. It requires aconsiderable skill and vigilance on the part of an auditor. Indoubtful cases he may refuse to believe the information suppliedto him by any officer of the concern.

An auditor who uses adequate skill and reasonable care, is legallyexempt from liability if he fails to discover a well concealeddetection. But an auditor by a skilled auditor should rarely permitsuch a failure.

6.12 O Solved Scanner IPCC Group- II Paper - 6

All possible opportunities for dishonesty and manipulation of theaccounts must be considered and guarded against and the degreeof checking and investigation should be determined by thecircumstances surrounding the transactions and the effectivenessof the system of intended check in operation.

(b) State clearly provisions of the Companies Act, 2013 with regard toissue of shares at a discount. (6 marks)Answer:Issue of Shares at a Discount:According to Sec. 53 of the Companies Act, 2013, except sweatequity issued as mentioned in Sec. 54, any share issued by acompany at a discounted price shall be void.Where a company contravenes the provisions of this section, thecompany shall be punishable with fine which shall not be less thanone lakh rupees but which may extend to five lakh rupees and everyofficer who is in default shall be punishable with imprisonment for aterm which may extend to six months or with fine which shall not beless than one lakh rupees but which may extend to five lakh rupees,or with both.

(c) What is the importance of having the accounts audited by anindependent auditor? (4 marks)Answer:

Independent Audit

1. Meaning Independence implies that the judgement of aperson is not subordinate to the wishes ordirections of another person who might haveengaged him or to his own self-interest.

2. Nature Independence is a condition of mind andpersonal character and should not be confusedwith the superficial and visible standards ofindependence, which are imposed by law.

Model Test Paper O 6.13

3. Visibility Independence of the auditor should not onlyexist, but should also appear to so exist to allreasonable persons. The relationshipmaintained by the auditor shall be such that noreasonable man can doubt his objectivity andintegrity. There is a collective aspect ofindependence that is important to theaccounting professional as a whole.

The advantages of an Independent Audit are :1. Protection of interest It safeguards the financial interest of

persons who are not associated withthe management of the organizationwhether they are partners orshareholders.

2. Moral check It acts as a moral check on theemployees from committingdefalcations.

3. Tax liability Audited statements of account arehelpful in setting liability for taxes.

4. Credit negotiation Financers and bankers use auditedfinancial statements in evaluating thecredit worthiness of individuals innegotiating loans.

5. Trade disputesettlement

Audited statements are useful insettling the trade disputes for higherwages, or bonus, etc.

6. Control overinefficiency

It helps in detection of wastages andlosses and also helps inrecommending ways to correct it.

7. Funds-in-trust It is an agency, which ensures thatpersons acting for others haveproperly accounted for the amountscollected by them.

6.14 O Solved Scanner IPCC Group- II Paper - 6

8. Arbitration It is helpful in settling disputes byarbitration.

9. Appraisal Audit reviews the existence andoperations of various controls in theorganization and reports inadequacies, weaknesses, etc inthem. Management can take suitableaction based on the reports.

10. Assistance togovernment

Government may require auditedand certified statements before itgives assistance or issues a licensefor a particular trade.

5. (a) Discuss the provisions of Section 134 of the Companies Act, 2013regarding the authentication of financial statements. (6 marks)Answer:As per provisions of Sec. 134(1), before submission to the auditorfor his report, the financial statements, including consolidatedfinancial statement, shall be approved by the Board of Directors:The signing of the financial statements shall be done:(a) by the chairperson of the company; where he is authorised by

the Board, or(b) by two directors out of which one shall be Managing Director.

And(a) The chief executive officer, if he is a director in the company,

wherever appointed.(b) The chief financial officer, wherever appointed and.(c) The Company Secretary of the company wherever appointed. In case of one Person Company, the financial statements shall

be signed only by one Director. A signed copy of every financial statement, including

consolidated financial statement, if any shall be issued,circulated or published along with copy of each of:(a) any notes annexed to or forming part of such financial

statements.

Model Test Paper O 6.15

(b) the Auditor’s Report, and.(c) the Board’s report referred u/s 134(3).

The auditor’s report shall be attached to every financialstatements as per Sec. 134(2).

(b) What are the duties of Comptroller and Auditor General?(6 marks)

Answer:The main duties of C & AG within the framework of theconstitution of India may be as follows1. Compilation and

submission ofAccounts

The C & AG should compile theaccounts pertaining to annual receiptsand disbursements of the Union orState or Union Territory and submitthese to the President or Governor orAdministrator.

2. RenderingAssistance inAccountsMaintenance

The C & AG should provide suchinformation to the Union or State asthey may require from time to time andrender such assistance for preparingannual financial statements as theyreasonably ask for.

3. Auditing andReporting

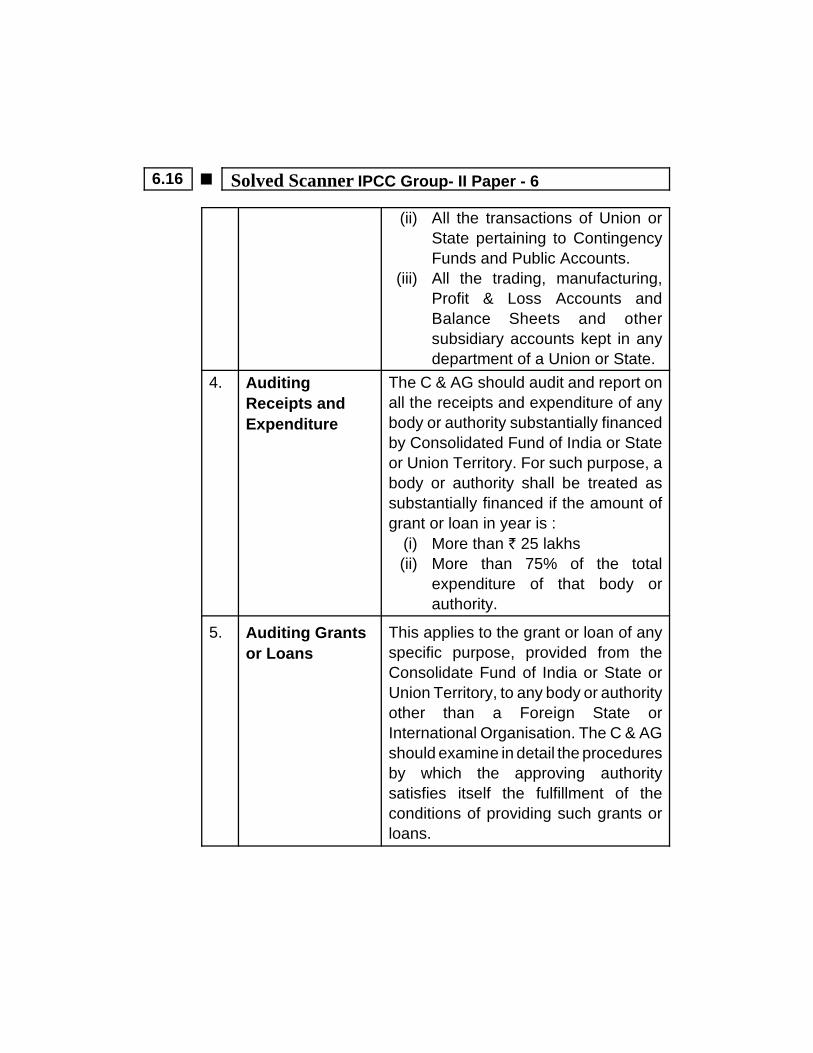

The C & AG should audit and reporton:

(i) All the expenditures fromC o n s o l i d a t e F u n d o fIndia/State/Union Territory havinga Legislative Assembly and todetermine whether the moniesdisbursed were legally availablefor and applicable to the purposeand service for which they areapplied and whether theexpenditures comply with theauthority governing it.

6.16 O Solved Scanner IPCC Group- II Paper - 6

(ii) All the transactions of Union orState pertaining to ContingencyFunds and Public Accounts.

(iii) All the trading, manufacturing,Profit & Loss Accounts andBalance Sheets and othersubsidiary accounts kept in anydepartment of a Union or State.

4. AuditingReceipts andExpenditure

The C & AG should audit and report onall the receipts and expenditure of anybody or authority substantially financedby Consolidated Fund of India or Stateor Union Territory. For such purpose, abody or authority shall be treated assubstantially financed if the amount ofgrant or loan in year is :

(i) More than ` 25 lakhs(ii) More than 75% of the total

expenditure of that body orauthority.

5. Auditing Grantsor Loans

This applies to the grant or loan of anyspecific purpose, provided from theConsolidate Fund of India or State orUnion Territory, to any body or authorityother than a Foreign State orInternational Organisation. The C & AGshould examine in detail the proceduresby which the approving authoritysatisfies itself the fulfillment of theconditions of providing such grants orloans.

Model Test Paper O 6.17

6. Auditing Receiptof Union orState

The C & AG should audit all thereceipts payable into the ConsolidatedFunds of India or State or UnionTerritory. He may satisfy himself thatthe rules and procedures have beendesigned to make an effective check onthe assessment, collection and properallocation of revenue and are dulybeing observed.

7. Auditing Storesand StockAccounts

The C & AG should be authorised toaudit and report on the stores and stockaccounts kept in any office ordepartment of the Union or State.

The C & AG should exercise suchpowers and duties according to theprovisions of Companies Act, 2013,pertaining to Government Companiesand Corporations.

(c) R.K. & Company are the auditors of PQR Company Ltd. TheManaging Director of the Company demands copies of the workingpapers from the auditors. Are the auditors bound to oblige theManaging Director? (4 marks)Answer:Working papers : Ownership and CustodyFacts : According to SA-230 “Audit Documentation”, the workingpapers are the property of the auditor, the auditor may, at hisdiscretion make portion of or extracts from his working papersavailable to the client.The auditor is entitled to retain them. (Chantrey Martin and Co. VsMartin)Analysis : In the given case the managing director of the companyhas demanded copies of the working papers from the auditor. He

6.18 O Solved Scanner IPCC Group- II Paper - 6

has no right to obtain copies of the working papers from the auditorbecause they are the property of the auditor. But the auditor may athis discretion make portions of or extracts from the working paper tothe managing director of R K & Company.Inference : The auditor is not bound to oblige the managing directorby supplying copies of the audit working papers.

6. (a) State any five special points which you, as an auditor, would lookinto while examining the income and collection of fund by an NGOengaged in providing relief work for flood victims. (6 marks)Answer:

Receipt of DonationsS.

No.Aspects to be

verifiedVerification

1. Internal Control Ensure that the internal control systemexists particularly referring the divisionof responsibilities with respect toauthorised collection of donation,custody of receipt books and safecustody of money.

2. Receipt BooksCustody

Ensure that unused receipt books arereturned and are verified physicallyincluding checking of number of receiptbooks and numbering sequencetherein.

3. Receipt ofCheque

Ensure that receipt book has a carboncopy for duplicate receipt and signed bya responsible official and also all detailspertaining to the date of cheque, bank’sname, date, amount etc. should beclearly indicated.

Model Test Paper O 6.19

4. Reconciliation ofBank Statement

Ensure reconciliation of bank statementwith reference to all cash depositsreferring to the date, amount and alsoreceipt book,

5. Receipt of Cash Ensure that registers of cash donationshave been vouched extensively.

6. Contributionsfrom Abroad

Any contribution made from abroadshould comply with the applicable lawsand regulations.

Remittance of DonationS.

No.Aspects to be

VerifiedVerification

1. Mode ofRemittance

All remittances are sent through A/cPayee Cheque. Remittance madethrough Demand Draft should alsobe scrutinized thoroughly withreference to recipient.

2. Confirmation ofReceipt ofRemittance

All remittances should have beensupported by receipts andacknowledgments.

3. Identity The recipient NGO is a genuineentity. The address, 80 GRegistration No., etc. should beverified.

4. Procedure of DirectConfirmation

Ensure that confirmation letters havebeen sent to those entities to whomdonation have been paid.

5. Use of Donation Ensure that donation has been usedfor the purpose required i.e. toprovide relief to Tsunami victims.

6. Selecting systemfor NGO

Ensure the system for selecting NGOto whom donations have been sent.

6.20 O Solved Scanner IPCC Group- II Paper - 6

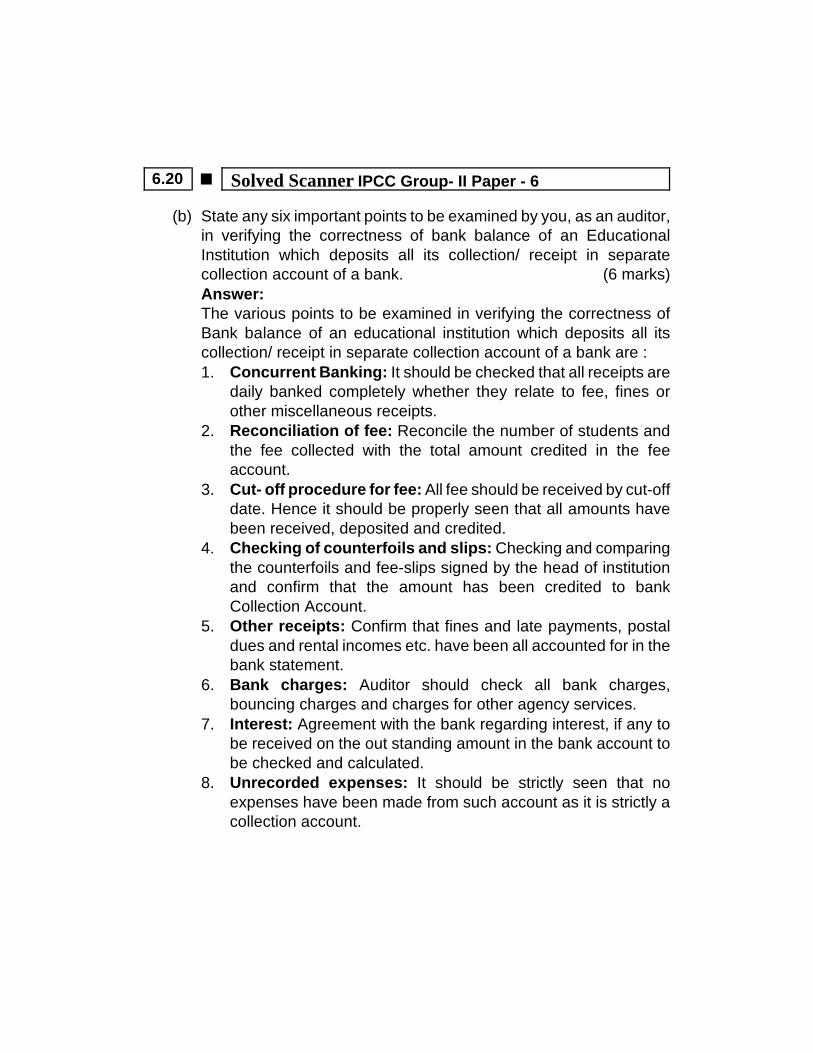

(b) State any six important points to be examined by you, as an auditor,in verifying the correctness of bank balance of an EducationalInstitution which deposits all its collection/ receipt in separatecollection account of a bank. (6 marks)Answer:The various points to be examined in verifying the correctness ofBank balance of an educational institution which deposits all itscollection/ receipt in separate collection account of a bank are :1. Concurrent Banking: It should be checked that all receipts are

daily banked completely whether they relate to fee, fines orother miscellaneous receipts.

2. Reconciliation of fee: Reconcile the number of students andthe fee collected with the total amount credited in the feeaccount.

3. Cut- off procedure for fee: All fee should be received by cut-offdate. Hence it should be properly seen that all amounts havebeen received, deposited and credited.

4. Checking of counterfoils and slips: Checking and comparingthe counterfoils and fee-slips signed by the head of institutionand confirm that the amount has been credited to bankCollection Account.

5. Other receipts: Confirm that fines and late payments, postaldues and rental incomes etc. have been all accounted for in thebank statement.

6. Bank charges: Auditor should check all bank charges,bouncing charges and charges for other agency services.

7. Interest: Agreement with the bank regarding interest, if any tobe received on the out standing amount in the bank account tobe checked and calculated.

8. Unrecorded expenses: It should be strictly seen that noexpenses have been made from such account as it is strictly acollection account.

Model Test Paper O 6.21

(c) Comment on the following situation:On 31.12.2008, Amudhan Company Limited has invested ` 45 lakhsin cumulative fixed deposits of Algar Bank Ltd. The deposits carryinterest @ 10% per annum compoundable quarterly and amount ofinterest is added to the principal and is due and payable at thematurity date which is 5 years from the date of investments.

For the year ended 31st March, 2009, the company did not bookany revenue of interest on the ground that interest amount is notavailable at their disposal till maturity date of investment.

(4 marks)Answer:(i) According to Sec. 148 of the Companies Act, 2013 books are to

be maintained on accrual basis. Accrual method of accountingis also a fundamental assumption of accounting policies.

(ii) When the interest becomes due for payment only at maturitydate, it accrues each quarter. Interest accrued but not dueshould be shown under current assets in the balance sheet asper Schedule III Part I requirement.

(iii) As such, the profits and current assets are understated and trueand fair view of the accounts are thus vitiated.

(iv) On considerations of materiality of the item, the auditor canappropriately decide to qualify the audit report.

7. Write short note on any four:(a) Reliability of audit evidences. (4 marks)

Answer:

Reliability ofAudit Evidence

SA 500 on “Audit Evidence” provides that thereliability of information to be used as auditevidence and therefore of the audit evidenceitself, is influenced by its source and its natureand the circumstances under which it isobtained, including the controls over itspreparation and maintenance where relevant.

6.22 O Solved Scanner IPCC Group- II Paper - 6

Therefore, generalisations about the reliability ofvarious kinds of audit evidence are subject toimportant exceptions. Even when information tobe used as audit evidence is obtained fromsources external to the entity, circumstancesmay exist that could affect its reliability.

The reliability ofaudit evidenceis influenced by

1. Its source i.e. internal and external.2. Its nature i.e. visual, documentary or oral.3. Circumstances under which it is obtained.4. Consistency of evidence obtained from

different sources or nature.5. Nature of assertion obtained and its

1. External evidence (e.g.: confirmationreceived from third party) is more reliablethan internal evidence.

2. Internal evidence is more reliable whenrelated internal control is satisfactory.

3. Evidence in the form of documents andwritten representations are usually morereliable than oral representation.

4. Evidence obtained by the auditor himself ismore reliable than that obtained through theentity.

(b) Write short note on Examination in depth. (4 marks)Answer:Examination in depth:Examination in Depth means an examination of a few selectedtransactions from the beginning to the end through the entire flow oftransaction. This examination includes studying, the recording oftransactions at each stage and judging, whether the person who hasexercised the authority in relation to the transaction is fit to do so.

Model Test Paper O 6.23

The selection must be correct and proper. A sample size may besmall but it should be a true representative of the universe oftransaction. Infact, the size depends upon the auditor’s ‘level ofconfidence’, there is a inverse relationship between them.For example: A purchase of goods may commence when thecompany reaches its re-order level.The probable steps of purchase are as follows :1. Requisition: pre-printed, pre-numbered, authorised.2. Formal purchase order: sequentially pre-numbered and

authorised- placed with the approved supplier only.3. Receipt of supplier’s invoice.4. Receipt of supplier’s statement.5. Entries made in purchase day book.6. Posting to purchase ledger and purchase ledger control A/c. and7. Cheque issued in settlement.8. Entry on bank statement and returned ‘paid’ cheque if

requested.9. Entry in cash book.10. Posting from cash book to ledger and it’s ledger control (taking

into account the discounts, if any).11. Receipt of goods, along with delivery or advice note.12. Issuance of goods received note and inspection certificate

containing initials or rubber stamp to show that goods areverified and inspected.

13. Admission of goods to store.14. Entries of goods to store.It should be kept in mind that the above list is not a fixed list and itssequence can be changed.So we can see that as soon as the company reaches the re-orderlevel, it has to follow a chain of events, also leaving an audit trail.Thus, examination in depth is necessary, as if it is conductedproperly, then it will reveal both the functioning or malfunctioning ofthe client’s system.

6.24 O Solved Scanner IPCC Group- II Paper - 6

(c) Reissue of redeemed debentures. (4 marks)Answer:Reissue of Redeemed Debentures1. See whether the expenses on re-issue are properly treated in

the accounts.2. Verify whether there is any alteration in the rights & privileges of

the Debenture holders in respect of debentures re-issued.3. See that the collateral security is disclosed against the liability

concerned in the inner column of Balance Sheet.(d) Defalcation of cash with examples. (4 marks)

Answer:Defalcation of CashDefalcation of cash may take place in following ways:1. By Inflating cash payment2. By suppressing cash receipts3. By casting wrong total in the cash book.The defalcation of cash is occurred due to the transactionaffecting the cash balances which are as follows: The cash payment made for purchases The payment made to supplier for credit purchases The payment made for expenses Cash in transit in case of consignment Bad debt incurred Purchase of fixed assets Redemption of debentures and buyback of the share capital Dividend paid for the year etc.

(e) Verification of credit sales. (4 marks)Answer:Verification of the credit sales : The credit sales should be verifiedby reference to copies of invoices issued to customers and, in theprocess.The Auditor should consider the following points:1. The credit sales should be verified by reference to copies of

invoices issued to customers and in the process, attentionshould be paid to the following matters:(i) that each item of sales relates to the period of account

under audit.

Model Test Paper O 6.25

(ii) that the goods are those that are normally dealt in by theconcern.

(iii) that the sale price has been correctly arrived at and thecopy of the requisition slip issued by the Sales Departmentand the copy of the Despatch Notes showing the date andmode of despatch of goods are attached with the invoice.

(iv) that the amount of the invoice has been adjusted in anappropriate account; and

(v) that the sale has been authorised by a responsible officialand in token thereof he has initialed the invoice also thatany alteration in the invoice has been attested by the sameperson.

2. If any additional charges are recovered along with the saleprice, these should be credited to separate accounts,appropriately headed, and not to the sales account.

3. When a trade discount is allowed, the amount thereof should bededucted from the sale price. When any special trade discounthas been allowed, the reason thereof should be ascertained.

4. Small concerns generally do not have well organised sales anddespatch departments. In such cases, for verifying sales theauditor should trace a small preparation of sales invoice into thestock book, specially of goods sold at the beginning and at theclose of the year.

5. The sale of goods on hire-purchase basis or goods sent out onsale or return basis or on consignment basis should beseparately recorded.

6. When credit sales are not adjusted in the account at the timethey are made but at the time sale proceeds are collected, therecan be no guarantee that any amount collected in such saleshas not been misappropriated. The auditor should, therefore,draw the attention of the management to the risk involved inadopting such practice.