Page 1

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

US PetrochemicalsThe growing importance of export markets

EIA Energy ConferenceJune 4, 2018

Blake Eskew, Vice President - Business Development Oil Markets / Midstream / Downstream / Chemicals Houston, TX [email protected]

Page 2

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Addressing strategic challenges with interconnected capabilities

Resources

Financial

Consolidated Markets & Solutions

Transportation

© 2017 IHS Markit. All Rights Reserved.

The comprehensive single source for global data & information, key market insights, analysis & forecasts

Page 3

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Core Segments within Energy & Natural Resources

• Country E&P Terms and Above-Ground Risk

• Plays and Basins• Costs and Technology• Companies and

Transactions

UPSTREAM

• Global Gas• Coal• Power and Renewables• Regional Gas, Power

and Coal Markets

POWER, GAS, COAL& RENEWABLES

• Long-Term Planning & Scenarios • Climate Strategy

• Curated Content• Integrated Energy Events & CERAWeek

ENERGY-WIDE PERSPECTIVES

• Crude Oil Markets• Midstream Oil and

Natural Gas Liquids• Refining and Marketing• Company Strategies and

Performance

OIL MARKETS, MIDSTREAM, DOWNSTREAM & CHEMICAL

• Chemical Week and Market Daily Service

• Base Chemicals & Plastics

• Specialty Chemicals• Costs & Technology• Company Benchmarking

& Analytics

Our core capabilities serve our energy and chemical customers across the value chain through focused data and insight subscriptions as well as consulting.

Page 4

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

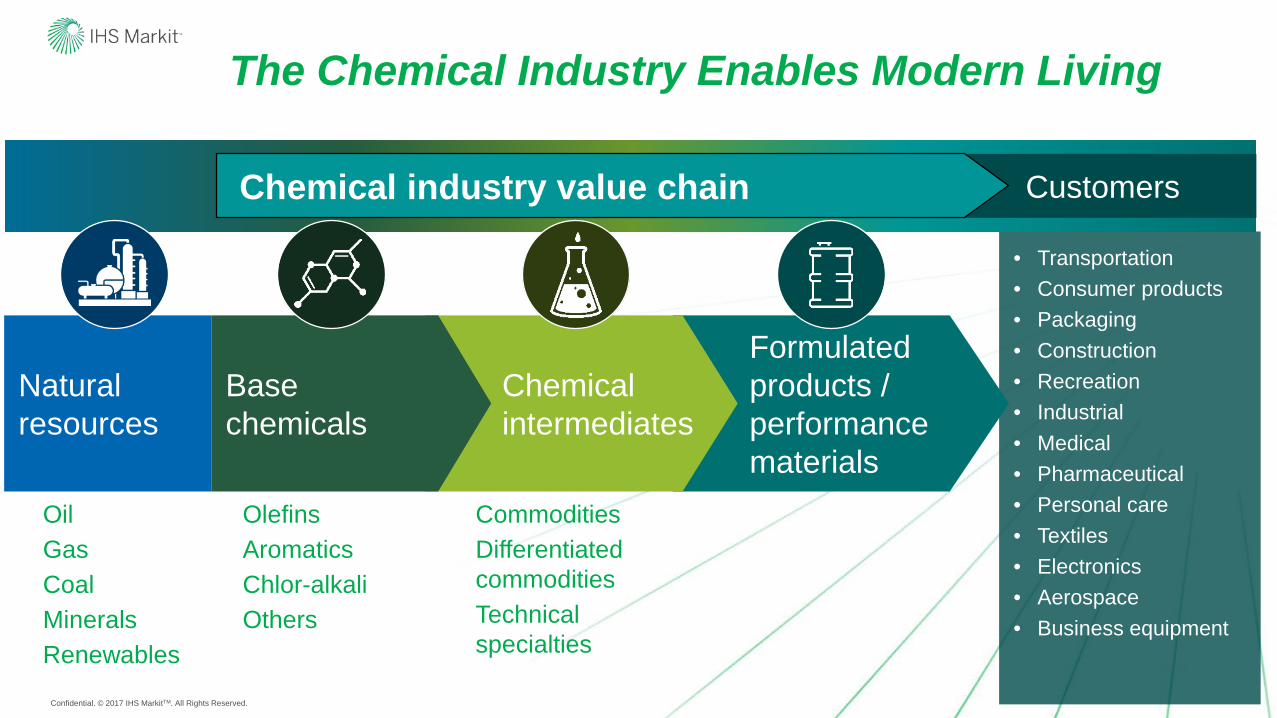

• Transportation• Consumer products• Packaging• Construction• Recreation• Industrial• Medical• Pharmaceutical• Personal care• Textiles• Electronics• Aerospace• Business equipment

OilGasCoalMineralsRenewables

Customers

Olefins AromaticsChlor-alkaliOthers

CommoditiesDifferentiated commoditiesTechnical specialties

Chemical industry value chain

Formulated products / performance materials

Natural resources

Chemicalintermediates

Base chemicals

The Chemical Industry Enables Modern Living

Page 5

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

-4

-2

0

2

4

6

8

10

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Perc

ent c

hang

e

World Advanced countries Emerging markets

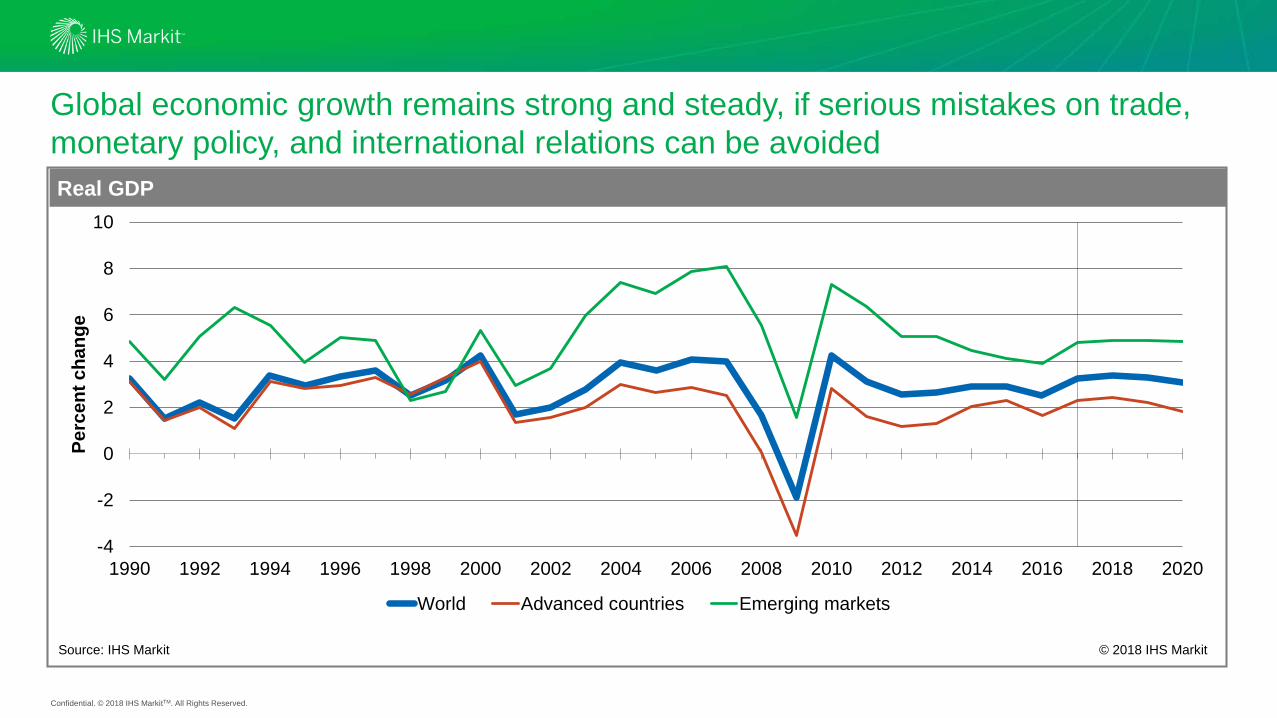

Global economic growth remains strong and steady, if serious mistakes on trade, monetary policy, and international relations can be avoidedReal GDP

Source: IHS Markit © 2018 IHS Markit

Page 6

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Economic growth in advanced countries and emerging markets are key drivers to petrochemical demand growth

0

1

2

3

4

1990-2000 2000-2010 2010-2020 2020-2030Ethylene Propylene (PG/CG) Methanol ChlorineBenzene Paraxylene Weighted Average

GDP Elasticity: rate of market growth / rate of global economic growth

Source: IHS Markit © 2018 IHS Markit

Per

cent

age

Page 7

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

1

2

3

4

5

6

7

Ethylene Propylene(PG/CG)

Methanol Chlorine Benzene Paraxylene

Avg. 2012 - 2016 2017 Avg. 2018 - 2022

Global demand growth and 2017 estimated total demand

Source: IHS Markit © 2018 IHS Markit

Mill

ion

Met

ric T

ons

Ethylene and propylene remain in high growth mode; methanol growth stabilizes

152 102

78 73

46 41

Global demand estimate for 2017

Page 8

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

The energy and petrochemical industries are closely related

Page 9

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

There are several primary routes to produce olefins

Crude Oil

Natural Gas

Crude Unit

Nat Gas Processing

FCC Unit

Refinery Grade Propylene

Ethylene

Polymer grade PropyleneSteam Cracker

PropyleneSplitter

PropaneDehydrogenation

Methanol-to-OlefinsMethanol-to-Propylene

Coal-to-OlefinsCoal-to-Propylene

Ethane, Propane, Butane

Propane

LPG, Naphtha, Gas Oil

Coal

Nat Gas

Page 10

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

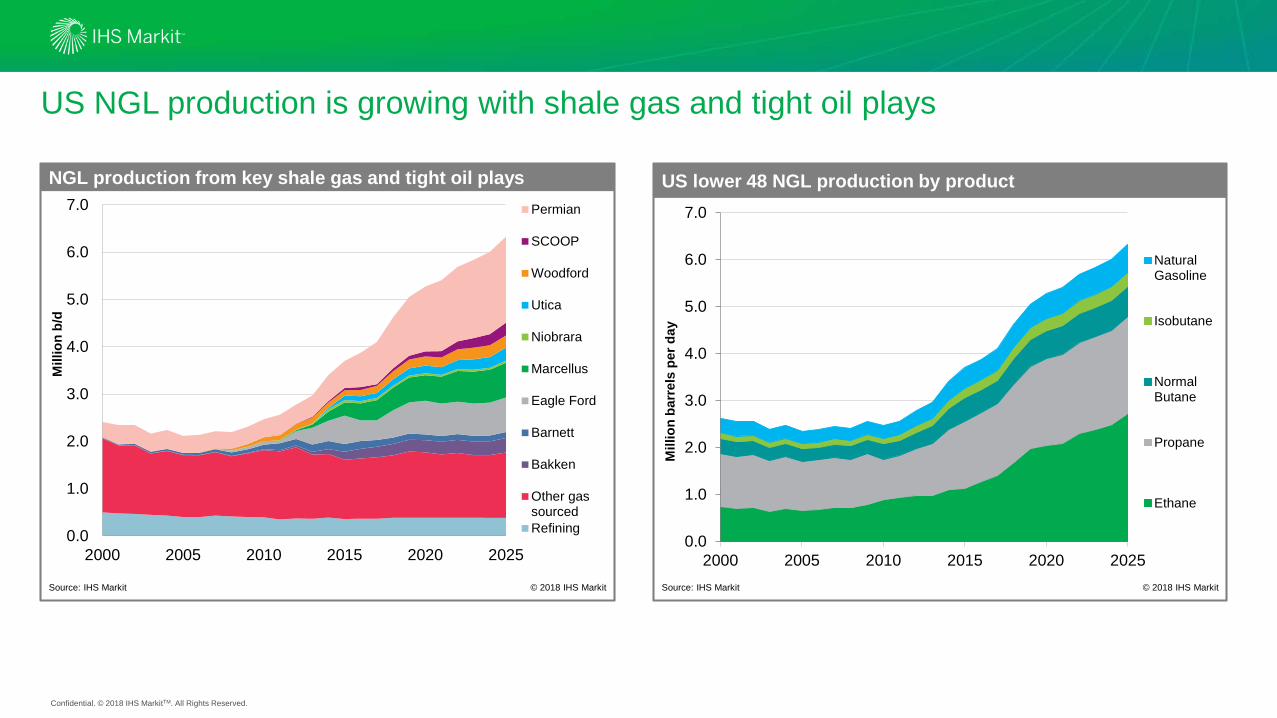

US NGL production is growing with shale gas and tight oil plays

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2000 2005 2010 2015 2020 2025

NaturalGasoline

Isobutane

NormalButane

Propane

Ethane

US lower 48 NGL production by product

Source: IHS Markit © 2018 IHS Markit

Mill

ion

barr

els

per d

ay

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2000 2005 2010 2015 2020 2025

Chart Title

Permian

SCOOP

Woodford

Utica

Niobrara

Marcellus

Eagle Ford

Barnett

Bakken

Other gassourcedRefining

NGL production from key shale gas and tight oil plays

Source: IHS Markit © 2018 IHS Markit

Mill

ion

b/d

Page 11

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

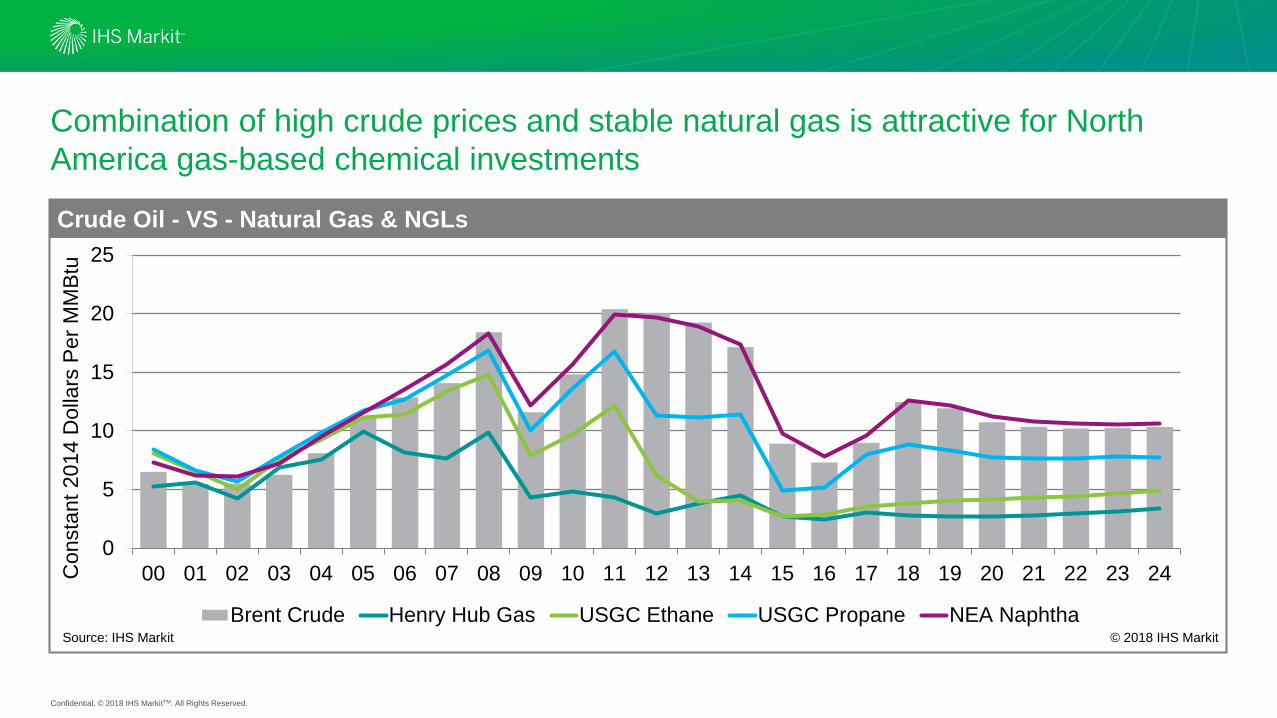

Combination of high crude prices and stable natural gas is attractive for North America gas-based chemical investments

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Brent Crude Henry Hub Gas USGC Ethane USGC Propane NEA Naphtha

Con

stan

t201

4 D

olla

rs P

er M

MB

tu

Crude Oil - VS - Natural Gas & NGLsCrude Oil - VS - Natural Gas & NGLsCrude Oil - VS - Natural Gas & NGLsCrude Oil - VS - Natural Gas & NGLs

Source: IHS Markit © 2018 IHS Markit

Page 12

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Ethane cracking is expected to maintain a large cash cost advantage

0

200

400

600

800

1000

1200

1400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017USGC - Ethane Northeast Asia - Naphtha

Ethylene Cast Cost Comparison

Source: IHS Markit © 2018 IHS Markit

USD

olla

r Per

Met

ric T

on

Cash cost = Feed + VC + FC – co-product

Page 13

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

63,832 57,481

21,706 9,812

Global Ethylene production by feed type (KTA ethylene by feed)

Source: IHS Markit © 2018 IHS Markit

Naphtha, 66,669

Ethane, 69,629

Other, 22,891

LPG, 13,383

NGLs increasingly important to olefins as crackers shift to ethane

0%

20%

40%

60%

80%

100%

2000 2003 2006 2009 2012 2015 2018 2021Gasoline (FCC) Naphtha Gas OilNat Gas Ethane PropaneButane Coal Other

Propylene production by feedstock

Source: IHS Markit © 2018 IHS Markit

Propane

More ethane for ethylene more propane for propylene

2017 (inner)Production = 143 MMTA

2022 (outer)Production = 173 MMTA

3.5 MMTA Ethylene~ 9 MMTA LPG

Page 14

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

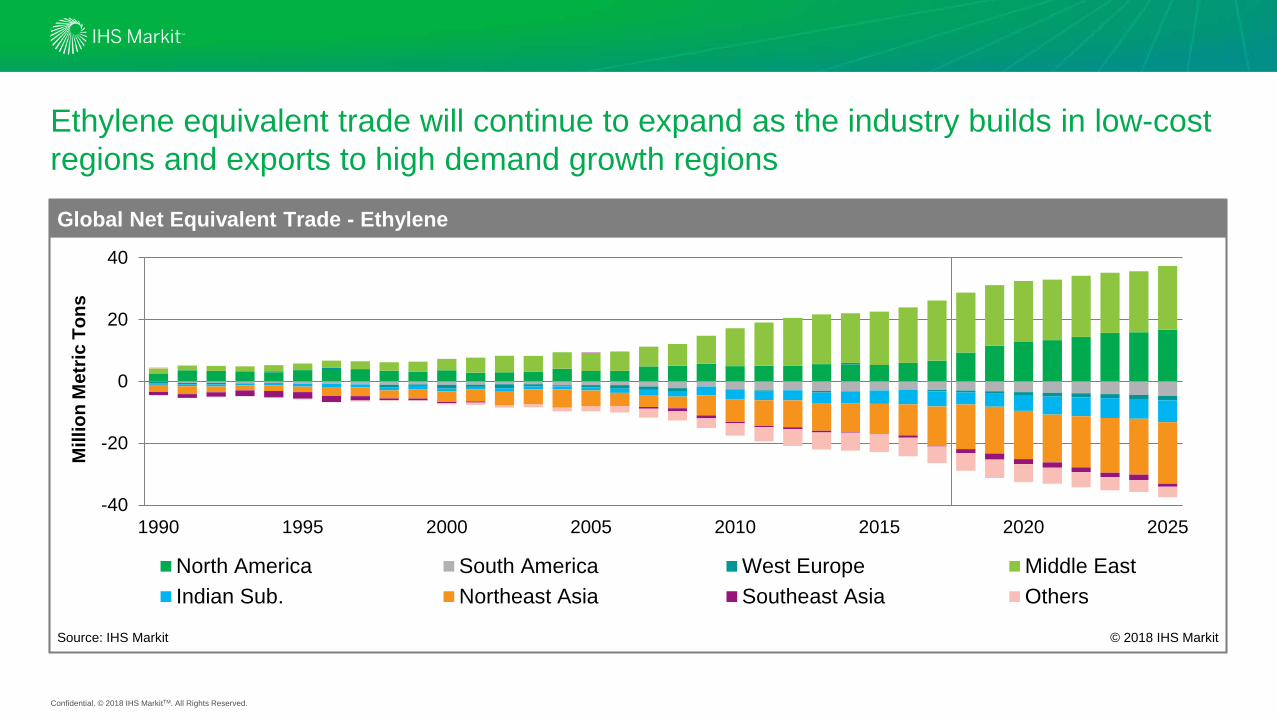

Ethylene equivalent trade will continue to expand as the industry builds in low-cost regions and exports to high demand growth regions

-40

-20

0

20

40

1990 1995 2000 2005 2010 2015 2020 2025

North America South America West Europe Middle EastIndian Sub. Northeast Asia Southeast Asia Others

Global Net Equivalent Trade - Ethylene

Source: IHS Markit © 2018 IHS Markit

Mill

ion

Met

ric T

ons

Page 15

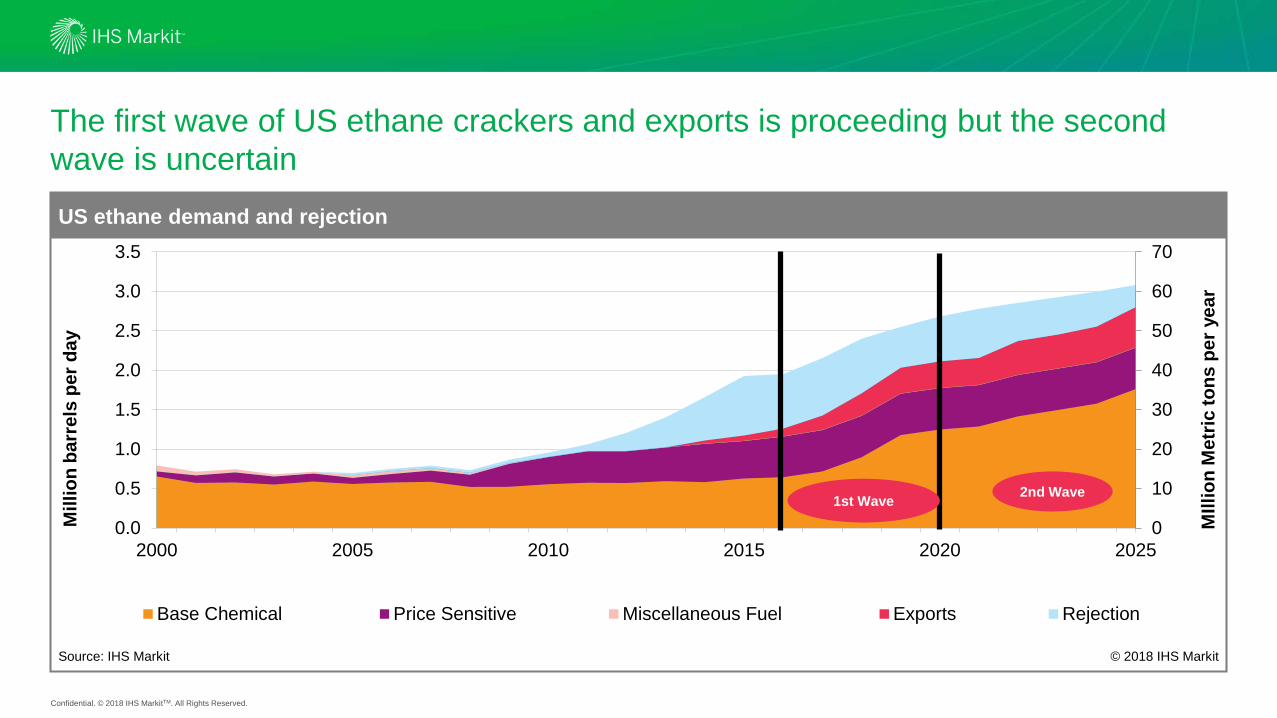

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

10

20

30

40

50

60

70

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000 2005 2010 2015 2020 2025

Chart Title

Base Chemical Price Sensitive Miscellaneous Fuel Exports Rejection

US ethane demand and rejection

Source: IHS Markit © 2018 IHS Markit

Mill

ion

barr

els

per d

ay

1st Wave 2nd Wave

MIll

ion

Met

ric to

ns p

er y

ear

The first wave of US ethane crackers and exports is proceeding but the second wave is uncertain

Page 16

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

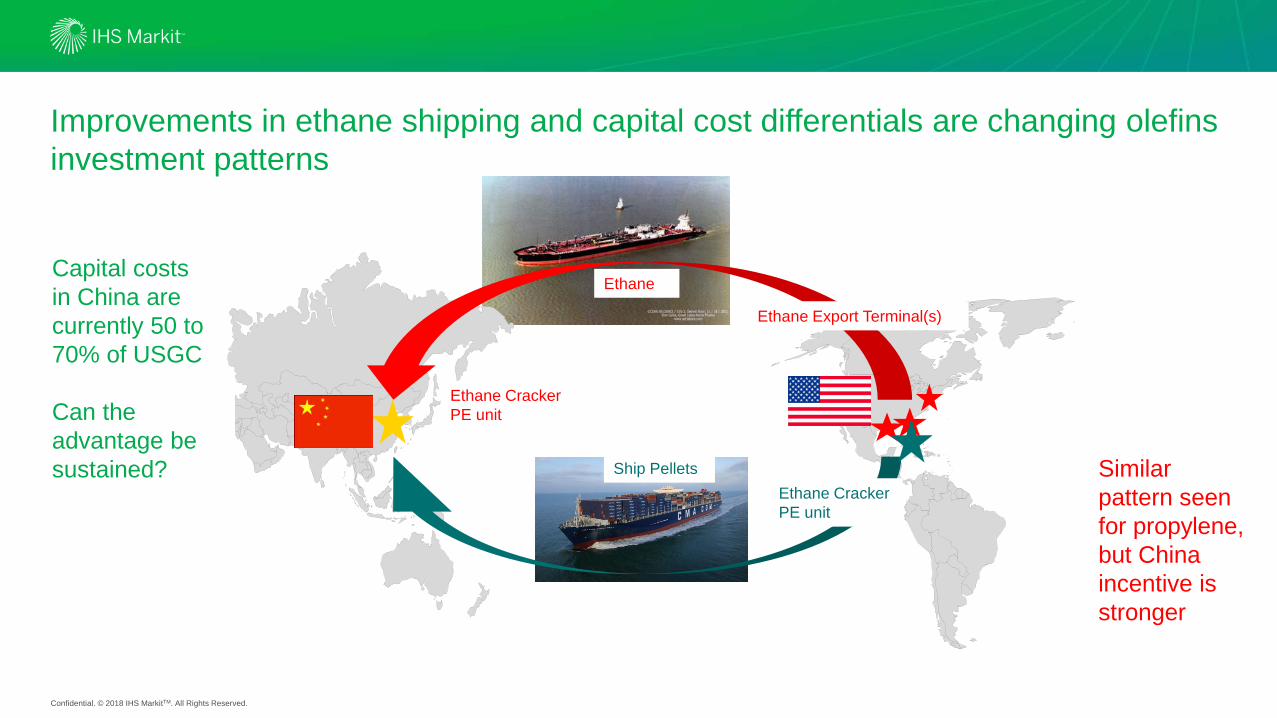

Improvements in ethane shipping and capital cost differentials are changing olefins investment patterns

Ethane Export Terminal(s)

Ethane CrackerPE unit

Ethane

Ship Pellets

Ethane CrackerPE unit

Capital costs in China are currently 50 to 70% of USGC

Can the advantage be sustained? Similar

pattern seen for propylene, but China incentive is stronger

Page 17

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Ethylene cash costs and capital cost advantages make Chinese ethane-based capacity competitive

0

100

200

300

400

500

600

700

800

USGC - Ethane China - Ethane from US China - Naphtha Europe - Naphtha

2020-2025 Average

2020-2025 Average

World Ethylene Cast Cost Comparison

Source: IHS Markit © 2018 IHS Markit

USD

olla

r Per

Met

ric T

on

Cash cost = Feed + VC + FC – co-product

• Cash costs for ethane cracking in China are higher than in the US due to ethane transport costs

• But - finished product shipping is reduced or eliminated

• In addition, capital cost savings may outweigh the higher operating and feedstock costs

• Ethane cracking capital cost in China is roughly half of naphtha cracking –economics depend on need for co-products

Page 18

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

NGL and mixed feed crackers dominate near-term capacity additions

• In addition, over 9 million tons of additional ethane-based units have been announced for China but are still in the planning stages

• In the US, almost 15 million tons of additional ethane-based capacity is under discussion

• With annual demand growth of 6 million tons, the capacity will be needed

• But – is there enough ethane? And where will it be built?

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

China India Other Asia Middle East Europe/CIS Africa North America

Ethane Other NGL Mixed Naphtha Other

World Ethylene Capacity Changes: 2017-2022

Source: IHS Markit © 2018 IHS Markit

Thou

sand

Met

ric T

ons

Page 19

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Energy and chemical exports from North America will continue to rise• Natural gas in North America remains

advantaged versus crude• North America will remain an attractive

region for capital investments in base chemicals, derivatives, and feedstocks

• Ethane to China can work - capital versus operating cost dynamics and supply risk tolerance will determine how much is built

• Second wave of ethane crackers will come – but in US or China?

• ,

19

Page 20

IHS Markit Customer [email protected] : +1 800 IHS CARE (+1 800 447 2273)Europe, Middle East, and Africa: +44 (0) 1344 328 300Asia and the Pacific Rim: +604 291 3600

DisclaimerThe information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2017, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.