37

From Technologies to Markets Advanced Packaging: Even Moore than you expect ! SEMICON EUROPA Thibault Buisson Business Unit Manager - [email protected] Grenoble | FR – October 26 th , 2016

From Technologies to Markets

Advanced Packaging:

Even Moore than you expect!

SEMICON EUROPA

Thibault Buisson

Business Unit Manager - [email protected]

Grenoble | FR– October 26th, 2016

2©2016 | www.yole.fr

PRESENTATION OUTLINE

oStatus of the Advanced Packaging• Market Dynamics, Drivers & Evolution of Semiconductor Packaging

• Advanced Packaging Platforms

• Market forecasts

• What about China?

• Key messages

oAn closer look on Fan-Out Packaging• Fan Out Applications

• Market trends

• Key messages

oConclusions

• Summary

3©2016 | www.yole.fr

PRESENTATION OUTLINE

oStatus of the Advanced Packaging• Market Dynamics, Drivers & Evolution of Semiconductor Packaging

• Advanced Packaging Platforms

• Market forecasts

• What about China?

• Key messages

oAn closer look on Fan-Out Packaging• Fan Out Applications

• Market trends

• Key messages

oConclusions

• Summary

4©2016 | www.yole.fr

Mainframe

Mini-computers

PCs

Desktop internet

Mobile Internet

Internet of Things

1MM+

10MM+

100MM+

1Bill+

10Bill+

10Bill+

1960 1970 1980 1990 2000 2010 2020 2030…

Smartphones/Tables

Industrial Applications

Automotive

Wearables and Health

Key Markets

Increased functionality

Increased performance

Miniaturization

Reduced Cost

Key Drivers

EVOLUTION of COMPUTING TRENDS & TODAY’s KEY MARKETS & DRIVERS

IoT / Wearables

5©2016 | www.yole.fr

Continuous performance advancements

SILICON/INTERCONNECTION TRENDS – “MORE MOORE” or even MOORE?

Production yields at advanced nodes are becoming more difficult => delaying commercialization of future technology nodes

6©2016 | www.yole.fr

THE EVOLUTION OF SEMICONDUCTOR PACKAGING

A bridging technology between ICs and PCBs

Packaging fillsthe gap in between ICsand PCBsdifferentspeeds of improvement

Feature sizes CMOS

transistors: 28nm

Feature sizes of PCBs

1970

Through

hole

technology

1980

Surface mount

devices

Deve

lopm

ent

in C

MO

S p

roce

ssin

g ca

pab

iliti

es

Deve

lopm

ent

in P

CB

pro

cess

ing

capab

iliti

es

1990

CSPs/BGAs

SiPs

2000

WLCSP

More SiPs

Flip Chip BGA

PoP

2010

3DIC TSV

Fan-out WLCSP

Cu pillars

Silicon interposers

7©2016 | www.yole.fr

THE EVOLUTION OF SEMICONDUCTOR PACKAGING

A bridging technology between ICs and PCBs

With spread of ICs in a variety of applications, numerousmarkets exist

Feature sizes of PCBs

…across several markets

Mobile:

High-end Multimedia

Smart-phones / PMP

High-density

Solid-State

Storage & µ-

Cards

Computing: Notebooks / MID

‘connectivity’ devices

Consumer:

Gaming / Graphic

application engines

Industrial:

HPC/ Network,

Servers

Consumer: High-performance

Digital Video

Wireless:

Connectivity /

Network

Center

Medical

Military & AerospaceTransportation:

Automotive,

Trains,

HEV/EV

Renewable Energy:

Photovoltains, Wind

Turbines…

Telecom: Power

Supplies…

Industrial

1970

Through

hole

technology

1980

Surface mount

devices

Deve

lopm

ent

in C

MO

S p

roce

ssin

g ca

pab

iliti

es

Deve

lopm

ent

in P

CB

pro

cess

ing

capab

iliti

es

1990

CSPs/BGAs

SiPs

2000

WLCSP

More SiPs

Flip Chip BGA

PoP

2010

3DIC TSV

Fan-out WLCSP

Cu pillars

Silicon interposers

8©2016 | www.yole.fr

FILLING THE SUBSTRATE DIMENSION GAP

Substrate manufacturers vs. Wafer foundries

Lower cost than

Si/Glass Interposer

100µm 10µm 1µm 100nm 10nm

PCB Design Rule Wafer Design Rule

Organic Substrate

GAP!

Silicon/Glass Interposer

~8-> 5µm

More functionalities and advanced technologies nodes

OSAT /

Wafer foundries

Substrate Manufacturers

High Cost

OPPORTUNITY!

WLP RDL

10©2016 | www.yole.fr

ADVANCED PACKAGING OVERVIEW 2014 vs. 2020

AP

38%

Other

62%

2014 Advanced Packaging REVENUE SPLIT

AP

19%

Other

81%

2014 Advanced Packaging WAFER SPLIT

AP

23%

Other

77%

2014 Advanced Packaging UNIT SPLIT

REVENUE split WAFER split UNITsplit2014

20

20 AP

44%

Other

56%

2020 Advanced Packaging REVENUE SPLIT

AP

30%

Other

70%

2020 Advanced Packaging UNIT SPLIT

AP

32%

Other

68%

2020 Advanced Packaging WAFER SPLIT

Growth of the Advanced Packaging!

300 mm eq. wafers *in billion units

20,2$B

33,3$B

30$B

38,3$B

17,2M

74,9M

40,6M

85M

52B

177,5B

102B

234B

In $B

11©2016 | www.yole.fr

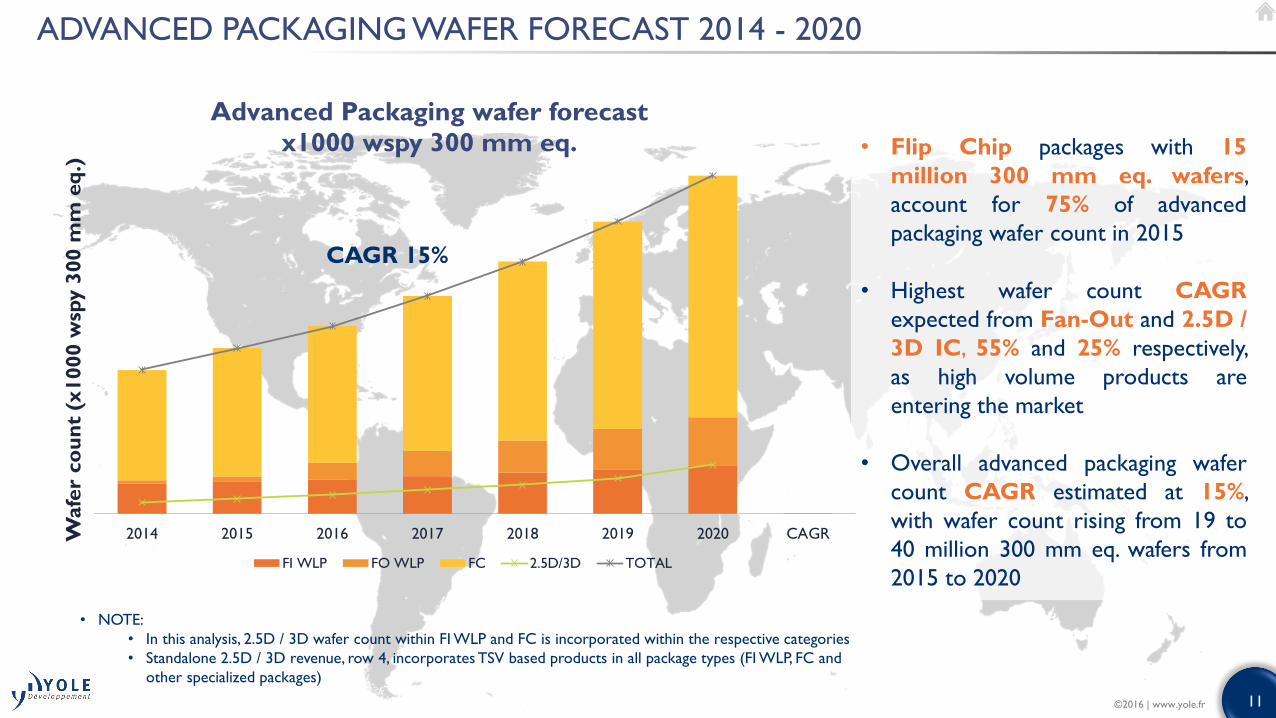

ADVANCED PACKAGING WAFER FORECAST 2014 - 2020

• Flip Chip packages with 15

million 300 mm eq. wafers,

account for 75% of advanced

packaging wafer count in 2015

• Highest wafer count CAGR

expected from Fan-Out and 2.5D /

3D IC, 55% and 25% respectively,

as high volume products are

entering the market

• Overall advanced packaging wafer

count CAGR estimated at 15%,

with wafer count rising from 19 to

40 million 300 mm eq. wafers from

2015 to 2020

• NOTE:

• In this analysis, 2.5D / 3D wafer count within FI WLP and FC is incorporated within the respective categories

• Standalone 2.5D / 3D revenue, row 4, incorporates TSV based products in all package types (FI WLP, FC and

other specialized packages)

CAGR 15%

2014 2015 2016 2017 2018 2019 2020 CAGRWafe

r co

un

t (x

1000 w

spy 3

00 m

m e

q.)

Advanced Packaging wafer forecast

x1000 wspy 300 mm eq.

FI WLP FO WLP FC 2.5D/3D TOTAL

12©2016 | www.yole.fr

ADVANCED PACKAGING REVENUE FORECAST 2014 vs. 2020

FI WLP

4 594

15%

FO WLP

2 391

8%

FC

23 034

77%

FI WLP

2 946

15% FO WLP

174

1%

FC

17 073

84%

TOTAL 2014

20,2 $B

TOTAL 2020

30 $B

• Due to faster growth, FO

WLP is expected to

decrease market shares of

Flip Chip

• FO WLP is expected to rise

from 1% advanced packaging

market share in 2014 to 8%

in 2020

• While maintaining growth,

from 2014 to 2020 Flip Chip

market share is expected to

drop from 84% to 77% while

FI WLP will remain at 15%

• NOTE: 2.5D / 3D revenue found within FI WLP and FC is incorporated within the respective categories

13©2016 | www.yole.fr

PLAYERS WITH ADVANCED PACKAGING CAPABILITY

Partial list

Key players in China with advanced packaging capability

Millenium Microtech Co. Ltd, bought

by FlipChip International, is now part of

Huatian. TianShui Huatian Technology

Co., LTD (“Huatian”) acquired FlipChip

International LLC and its subsidiary,

Millennium Microtech (Shanghai) Co.,

LTD, on Apr.1, 2015.

IDM

14©2016 | www.yole.fr

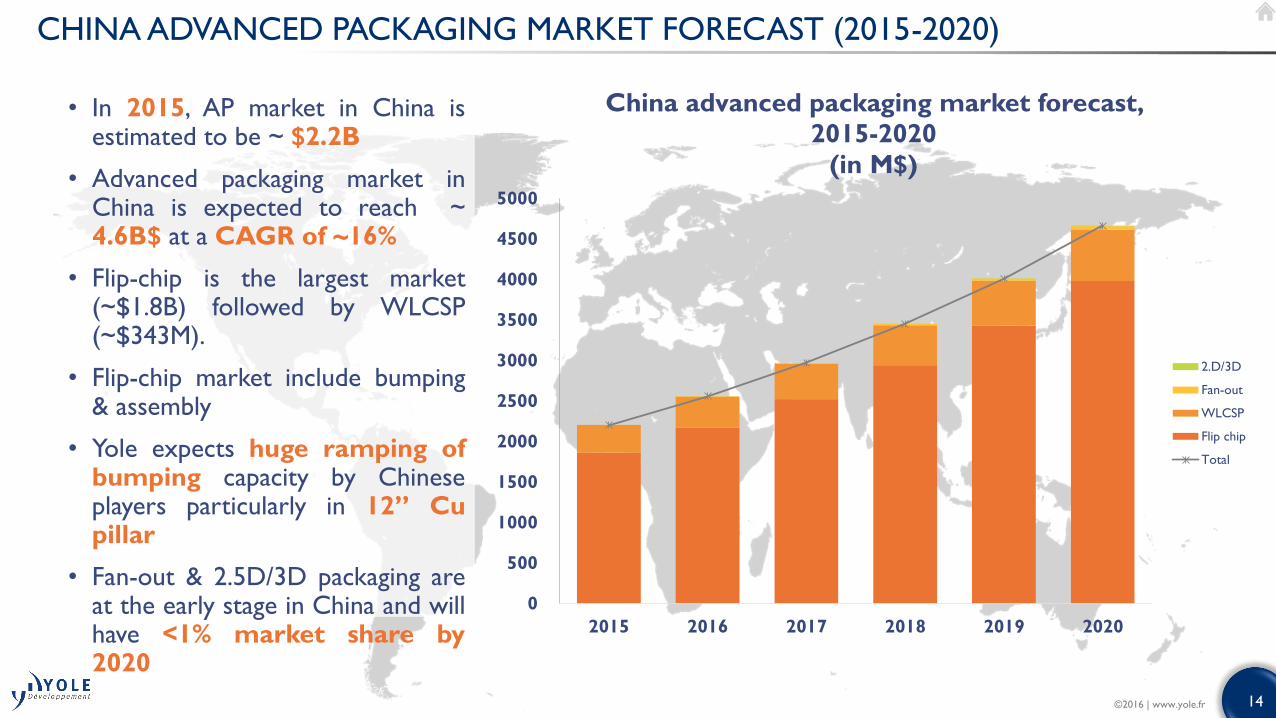

CHINA ADVANCED PACKAGING MARKET FORECAST (2015-2020)

• In 2015, AP market in China isestimated to be ~ $2.2B

• Advanced packaging market inChina is expected to reach ~4.6B$ at a CAGR of ~16%

• Flip-chip is the largest market(~$1.8B) followed by WLCSP(~$343M).

• Flip-chip market include bumping& assembly

• Yole expects huge ramping ofbumping capacity by Chineseplayers particularly in 12” Cupillar

• Fan-out & 2.5D/3D packaging areat the early stage in China and willhave <1% market share by2020

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2015 2016 2017 2018 2019 2020

China advanced packaging market forecast,

2015-2020

(in M$)

2.D/3D

Fan-out

WLCSP

Flip chip

Total

15©2016 | www.yole.fr

ADVANCED PACKAGING MARKET IN CHINA – THE RISE OF CHINA

0

5000

10000

15000

20000

25000

30000

35000

2015 2016 2017 2018 2019 2020

Advanced packaging market forecast, 2015-2020

(Global vs China) – Market (M$)

Global

China

• AP in China is expected to growat double CAGR (~16%)compared to 7% globally

• The growth in China AP is led byJCET/STATSChipPAC, Huatian,NFME, and China WLCSP

• After acquiring STATSChipPAC,JCET is the #4 OSAT in revenueglobally

• Global OSATs like Amkor and SPILare investing in the AP capability oftheir Chinese operations

• Amkor China (Shanghai) operationis the Amkor’s second-largestfactory by revenue"

16©2016 | www.yole.fr

ADVANCED PACKAGING - KEY MESSAGES

• Scaling of transistors is getting more and more complex. To enable solutions, focusis therefore on Advanced Packaging throught different platforms

• Advanced Packaging will keep growing in the next five years from 20B$ up to 30B$in 2020.

• Fan Out packaging is expected to have the fastest growth with a CAGR of 55%from 2015 to 2020 mainly due to its adoption in consumer market (Apple entry)

• 3D is getting is era in the high end application. Stacked memories will become key forhigh performance devices

• Advanced Packaging in China will grow faster (16%) compare to the global trendhowever emerging platforms are still at the early stage (3D, Fan Out.)

17©2016 | www.yole.fr

PRESENTATION OUTLINE

oStatus of Advanced Packaging• Market Dynamics, Drivers & Evolution of Semiconductor Packaging

• Advanced Packaging Platforms

• Market forecasts

• What about China?

• Key messages

oAn closer look on Fan-Out Packaging• Fan Out Applications

• Market trends

• Key messages

oConclusions

• Summary

18©2016 | www.yole.fr

KEY APPLICATIONS

Different applications with different needs and characteristics (Density, package size)

Codec

DC-DC

Wifi

BB

PMU/PMIC

RF

Application

Processors (APE)

+ BB

APE+DRAM

GPU, CPU + Memory

(Wide IO, etc…)

High Bandwidth

Memories

FPGA

Processors + Memories

IO density (IO/mm/layer)

200

100

1

2x2 5x5 10x10 15x15 20x20 >20x20 >>20x20 Package size

(mmxmm)

MEMS

CMOS Image Sensors

Display Drivers

10

>>200

19©2016 | www.yole.fr

MEMS

CMOS Image Sensors

Display Drivers

Codec

DC-DC

Wifi

BB

PMU/PMIC

RF

Application

Processors

(APE) + BB

APE+DRAM

GPU,CPU+Memory

(Wide IO, etc…)

High Bandwith Memories

FPGA

Processors+Memories

FAN-OUT APPLICATIONS

Potential applications for Fan-Out: Where does Fan-Out fit and how?

Single Chip FOWLP

Multi-Chip

FO PoP with TMV

FO SiP

Multi-Chip

FO PoP with TMV

IO count10000

1000

100

2x2 5x5 10x10 15x15 20x20 >20x20 >>20x20

Package

size

(mmxmm)

20

FAN-OUT APPLICATIONS

Where can we and will we find Fan-Out? Some examples below

Orange: Devices that can be found in

FOWLP packages today

Green: Devices that could be found

in the future in FOWLPGrey: Devices that will likely remain

on WLCSP or flip-chip package or

move to 3DIC or Embedded die

Apple iPhone 7 (2016)A10 APE – InFO package (TSMC)

Samsung Galaxy S7 (2016)Qualcomm Audio Codec

WCD9335 – eWLB package

(Nanium/STATS ChipPAC)

Bosch MRR1Plus Radar (2015)Infineon RASIC™ (77GHz RADAR System

IC Chipset) – eWLB Package

BK Ultrasound Sonic Window (2015)Multichip Module – eWLB Package (Nanium)

BasebandSpreadtrumSC8502

Intel-Mobile/InfineonPMB7900, PMB9810, PMB9801

RFSpreadtrumSC8502

Intel-Mobile/InfineonPMB5712, PMB5726 Power Management

MarvellPM820

SpreadtrumSC2712A

Continental ARS400 Radar (2015)NXP MR2001 (77GHz multichannel

RADAR) – RCP Package

©2016 | www.yole.fr | Yole Développement

21©2016 | www.yole.fr

APE

FAN-OUT APPLICATIONS

Example of Qualcomm’s Audio Codec

WCD9335 – eWLB package

Die size: 3.6x3.6mm² Package size:

4.18x3.91mm² 113 balls bumped

Source: System + Consulting

Audio codecRF in automotive

TSMC’s InFO for Apple A10Example of Infineon’s Transceiver

and Receiver in Bosch MRR1 Plus

Radar – eWLB packages

Source: System + Consulting

2012 2013 20142011 2015 2016

22©2016 | www.yole.fr

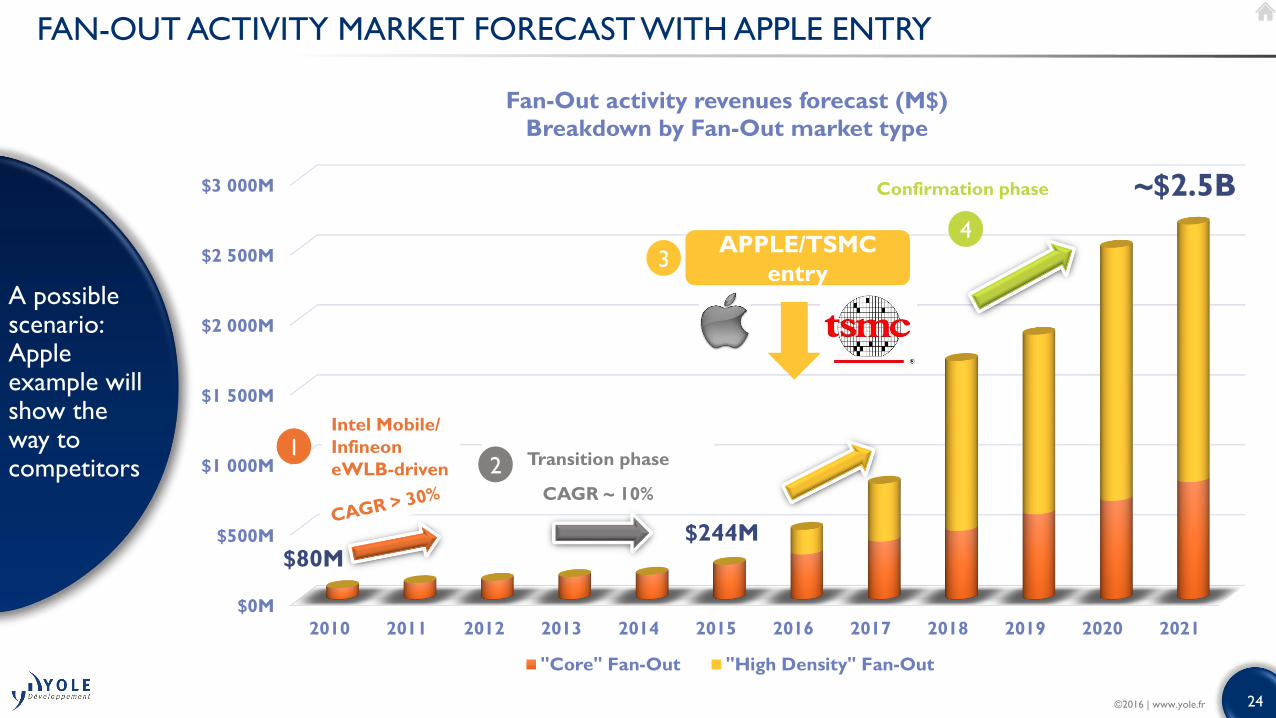

FAN-OUT MARKET STATUS

Entering a new era…

• A confirmed ramp-up and high expectations for a promising“core” market.

• A high potential for “High-Density” Fan-Out

Fan-Out market has reached a turning point • Is there a Fan-Out Bubble?

• Fan-Out is the new trendy platform the industry is focusing on…

• … but main part of Fan-Out Market for 2016 will be associated to only one product

23©2016 | www.yole.fr

IS THERE A FAN-OUT BUBBLE?

Fan-Out market risks

• Heavy competition pushed by substrates manufacturers may limit its success

High expectations induce risks

• Fan-Out market may not be not as sustainable as it seems: Few players dependency

24©2016 | www.yole.fr

$0M

$500M

$1 000M

$1 500M

$2 000M

$2 500M

$3 000M

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Fan-Out activity revenues forecast (M$)

Breakdown by Fan-Out market type

"Core" Fan-Out "High Density" Fan-Out

FAN-OUT ACTIVITY MARKET FORECAST WITH APPLE ENTRY

A possible scenario: Apple example willshow the way to competitors

APPLE/TSMC

entry

CAGR ~ 10%

Intel Mobile/

Infineon

eWLB-drivenTransition phase

12

3

4

~$2.5B

$80M$244M

Confirmation phase

25©2016 | www.yole.fr

FAN-OUT PACKAGING 2015 REVENUES MARKET SHARES (IN M$)

2015 FOWLP marketstatus shows a domination of twoplayers usingeWLB

59%25%

16%

Main products:

- eWLB single die packages for

Mobile and Wireless BB

and Wireless SoC, RF, PMIC

- MCP/SiP products for Mobile

(PMU), Industrial, Medical and

Security applications

eWLB products mainly

for

- Mobile and Wireless

BB and Wireless SoC

- PMU/PMIC

- RF

Others

TOTAL 2015

$244M

26©2016 | www.yole.fr

37%

12%

35%

16%

FAN-OUT PACKAGING 2016 REVENUES MARKET SHARES (IN M$)

2016 Fan-Out marketstatus shows TSMC entry and inFOtake over

TOTAL 2016

$492M

2016: Apple A10 entry with TSMC info will change the Fan-Out market landscape!

Others

27©2016 | www.yole.fr

FAN-OUT TECHNOLOGIES VS OTHER TECHNOLOGIES

A subtile trade-off between cost, performance and integration, case by case

DRAMDRAM

• Solution supplied by TSMC for Apple A10

Fan-Out PoP Flip Chip PoP Embedded die PoP

• Solution supplied by Samsung for its Exynos 8

• Solution supplied by Shinko for Qualcomm’s Snapdragon 820

28©2016 | www.yole.fr

FAN-OUT PACKAGING: AN EVOLUTION NOT A REVOLUTION

• Fan-Out packaging has numerous added values (form factor, electrical performance,…)

• Fan-Out Packaging is already adopted by the industry and will keep growing

• Following that success numerous players entered the game and provided newtechnologies inducing some confusion on what is “Fan-Out”

• Apple entry using TSMC InFo has changed the game and may have created a bubble…

• ~150$M loss is expected for substrate manufacturers in the 2 coming years.

• … but the market will enlarge anyway since it has high potential in telecom, medical andautomotive

29©2016 | www.yole.fr

PRESENTATION OUTLINE

oStatus of Advanced Packaging• Market Dynamics, Drivers & Evolution of Semiconductor Packaging

• Advanced Packaging Platforms

• Market forecasts

• What about China?

• Key messages

oAn closer look on Fan-Out Packaging• Fan Out Applications

• Market trends

• Key messages

oConclusions

• Summary

30©2016 | www.yole.fr

CONCLUSION: ADVANCED PACKAGING OVERVIEW

• Fan-in – stable growth, still driven by low cost and introduction of new

consumer applications (IoT) requiring low cost and pin count

• Flip-chip – will continue to grow, but expected to loose overall market

share to platforms such as WLCSP, Fan-Out and 3DIC. Cu Pillar will

continue to be the dominant flip chip metallurgy

• Fan-Out – very promising platforms already established in production.

Currently using wafer infrastructure, may move to panel manufacturing in

near future. Fan-out could be a disruptive technology for consumer

applications

• 2.5D & 3DIC – finally in production and adoption expected to further

grow. After MEMS and CIS, Memory will be the next segment to see the

growth and adoption of TSV.

• Advanced Substrates / SiP – enabling increased functionality solutions,

is a high interest packaging approach, especially driven by IoT (wearables)

RF applications and automotive

31©2016 | www.yole.fr

CONLUSION: ADVANCED PACKAGING OVERVIEW

ADVANCED PACKAGING is KEY

for the FUTURE!

THANKYOU for your attention!

32©2016 | www.yole.fr

INFORMATION EXTRATED FROMYOLE REPORTS

+ Several reports from System Plus Consulting & Knowmade

http://www.i-micronews.comMeet with the analysts at our BOOTH #850

Yole DéveloppementCompany Presentation

Light festival in Lyon

34

MEMS &

Sensors

LED

Compound

Semi.

Imaging

RF

MedTech

Manufacturing

Advanced Packaging

Batteries / Energy

Management

Power

Electronics

FIELDS OF EXPERTISE

Yole Développement’s 30 analysts operate in the following areas

Advanced Packaging and Manufacturing Business Unit

Photonics

35

4 BUSINESS MODELS

o Consulting and Analysis

• Market data & research, marketing analysis

• Technology analysis

• Strategy consulting

• Reverse engineering & costing

• Patent analysis

www.yole.fr

o Reports

• Market & Technology reports

• Patent Investigation and patent infringement risk analysis

• Teardowns & Reverse Costing Analysis

• Cost Simulation Tool

www.i-Micronews.com/reports

o Financial services

• M&A (buying and selling)

• Due diligence

• Fundraising

• Maturation of companies

• IP portfolio management & optimization

www.yolefinance.com

www.bmorpho.com

o Media

• i-Micronews.com website

• @Micronews e-newsletter

• Communication & webcast services

• Events

www.i-Micronews.com

Advanced Packaging and Manufacturing Business Unit

36

A GROUP OF COMPANIES

Market,

technology and

strategy

consulting

www.yole.fr

M&A operations

Due diligences

www.yolefinance.com

Innovation and business maker

www.bmorpho.com

Manufacturing costs analysis

Teardown and reverse engineering

Cost simulation tools

www.systemplus.fr

IP analysis

Patent assessment

www.knowmade.fr

Advanced Packaging and Manufacturing Business Unit

37

OUR GLOBAL ACTIVITY

Advanced Packaging and Manufacturing Business Unit