45

XBRL Implementation in IDX Februari 2014

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | joan-blankenship |

| View: | 221 times |

| Download: | 0 times |

XBRL Implementation in IDX Februari 2014

2

Today’s Discussion

• Introduction to XBRL• XBRL Implementation at IDX • More Details about IDX Taxonomy• Feedback• Q & A

3

Introduction to XBRL

What is XBRL ?

4

Allows Customisation

of Concepts

Uniquely Defined

Concepts

Computer Understandable

Language

An Information Standard

XBRL – The “Bar Code” for Business Reporting World

How XBRL Works?

• The main purpose of XBRL is how business and financial data can be easily exchanged, compared and utilized without any constraints of Accounting Standard or language barrier.

• XBRL works by creating a sign (called “tag”) which can be identified specifically for each data. This Tag can be easily read by a computer software so that the data could be identified in any language.

• This method will simplify other parties in gathering and processing data electronically without the need to translate and re-keying of data. It will be easier in comparing data because of the similar tags used in reporting.

6

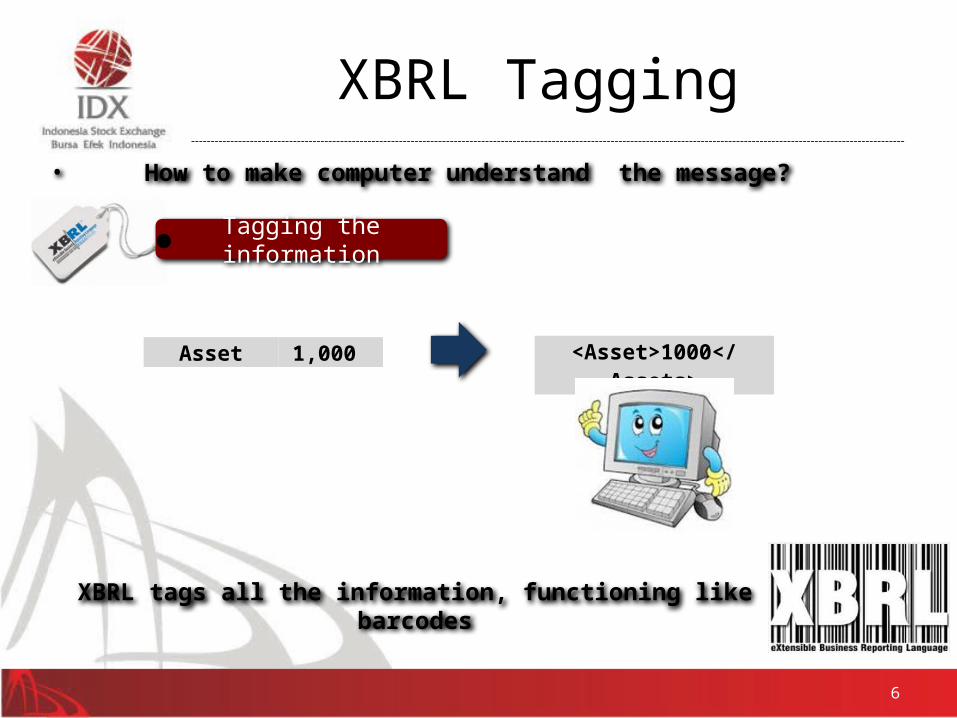

XBRL Tagging • How to make computer understand the message?

Tagging the information

Asset 1,000 <Asset>1000</Assets>

XBRL tags all the information, functioning like barcodes

Reporting Before XBRL

Source Formats Receivers

7

Financial System

Explanatory Disclosure

Reporting after XBRL

Source Formats Receivers

8

Financial System

Explanatory Disclosure

XBRL generalizes all reporting languages into 1 standard report

• Improves access to financial information

• Facilitates comparison & analysis• Improves accuracy of financial

data & reduces costs• Allows for open financial

reporting frameworks

The Advantages of XBRL

• Improve analysis of reports• Cost savings• Faster, more accurate and reliable• Decrease manual comparison among reports• Decrease Data Re-Entry• Improve dissemination of information on the Internet• Standardized reporting format

Who will benefit from using XBRL?

• Companies who prepare financial statements: More efficient preparation of financial statements because the reports will be created one time and rendered as printed reports, on Web sites or as other regulatory filings.

• Analysts, Investors, and Regulators: Enhanced distribution and usability of existing financial statement information. Automated analysis, significantly reduces re-keying of financial information from one form into another form, receiving information in the format that is more preferable for specific style of analysis.

• Financial publishers and data aggregators: More efficient data collection lowers operating costs associated with custom, idiosyncratic data feeds and reducing errors while concentrating on adding value to the data and increasing transaction capacity

• Independent Software Vendors: Virtually any software product that manages financial information can use XBRL for its data export and import formats, thereby increasing its potential for full-interoperability with other financial and analytical applications.

10

Source: www.accountingweb.com

11

XBRL Usage

source: http://www.xbrl.org/knowledge_centre/projects/mapCurrently XBRL has been adopted as standard reporting over the globe

12

XBRL Components

13

XBRL IMPLEMENTATION at IDX

Background

Monitoring Perspective• Responsive monitoring requires better, faster, & reliable information

management because :– More companies listed on IDX– More dynamics and complexities of corporate actions– More types of reporting and disclosure– More types of securities and type of issuer

• Enhancing monitoring ability by creating Business intelegence.

Quality of Disclosure Perspective• More reliable and informative disclosure of listed company needed by

market and investor• Differences of languages and financial standards between global investors

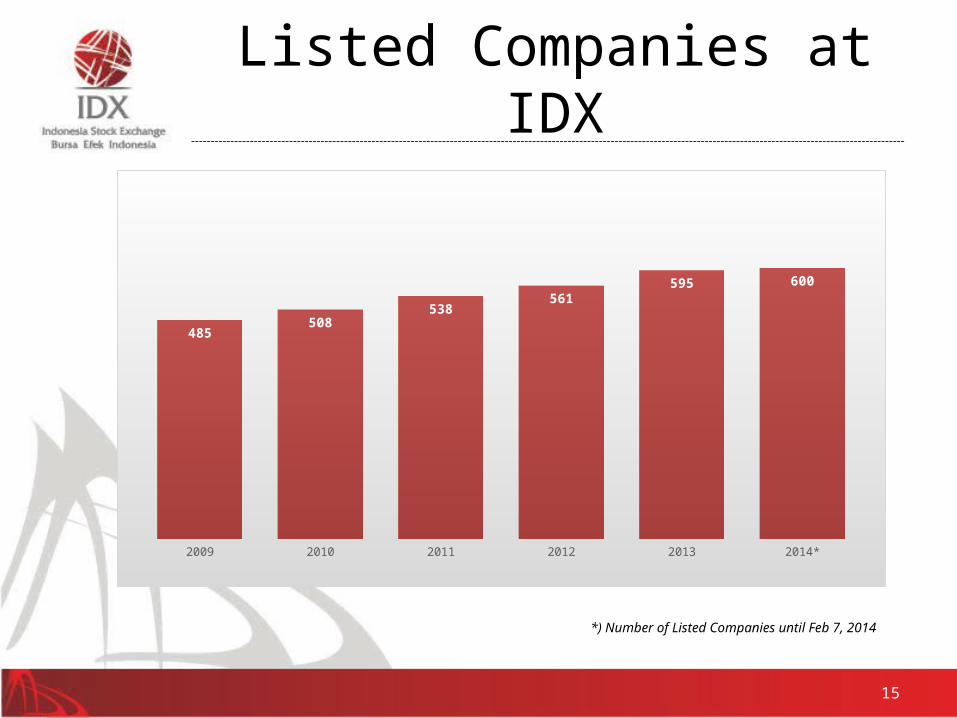

Listed Companies at IDX

15

*) Number of Listed Companies until Feb 7, 2014

2009 2010 2011 2012 2013 2014*

485508

538561

595 600

Number of Listed Shares by Industry

16

Finance81

16%

Trade, Services & Investment

11022%

Agriculture204%

Mining398%

Basic Indus-try & Chem-

icals61

12%

Miscella-neous Indus-

try418%

Consumer Goods Indus-

try388%

Property, Real Estate & Construc-

tion54

11%

Infrastructure, Utilities & Transporta-tion48

10%

Electronic Reporting System IDXnet

• IDXNet are electronic reporting system for listed companies, and monitoring of listed companies as well

• IDXNet accessible through public internet • IDXNet 1st generation based on XML Form launch at January 2009,

used only for equity issuer.• IDXNet 2nd generation based on both PDF Form and XML database

launched on March 2013, also used for Bonds, Sukuk, ABS, ETF and SPEI Issuer. OJK is also targeting to implement an equivalent system as IDXnet in 2013.

Jan 20091st generation IDXnet

Mar 2013New generation

IDXnet

Future DevelopmentXBRL Form Support

IDXnet 3rd Generation – XBRL Adoption (Plan)

18

Planning of XBRL Implementation in IDX

Build Taxonomy

Expand Scope of XBRL Adoption

Provide Solution

Publication and Recognition

Implementation

2013 2014 2015

Financial Statementwithout Disclosure

Notes

Financial StatementDisclosure

Financial Statementwithout Disclosure

Financial Statementwithout Disclosure

Financial Statementwithout Disclosure

20

More Details About IDX Taxonomy

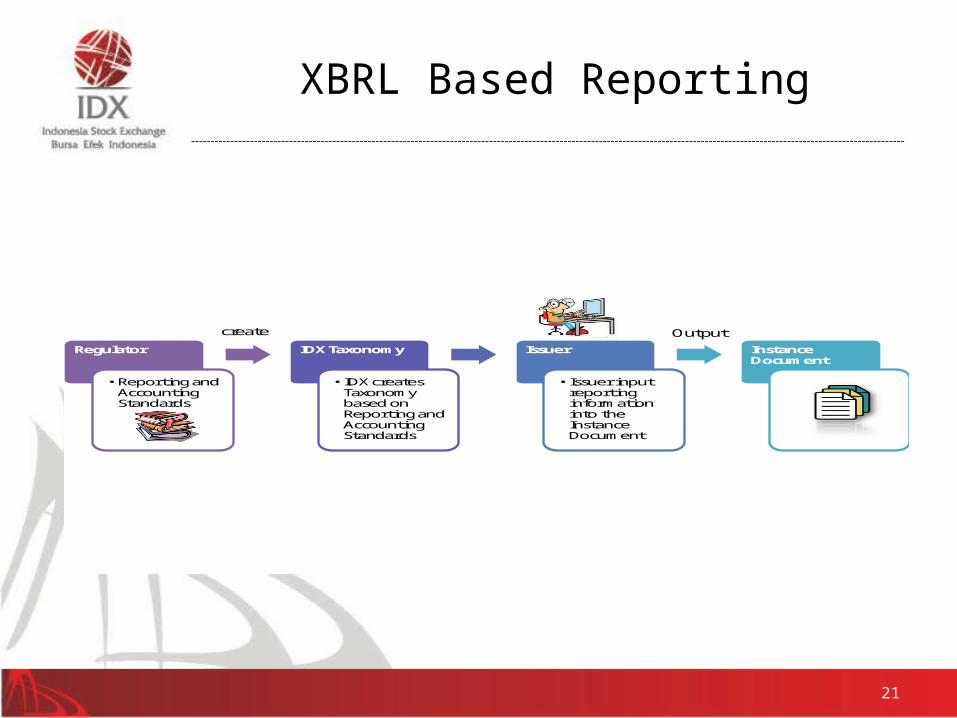

XBRL Based Reporting

21

Regulator

•Reporting and Accounting Standards

IDX Taxonomy

•IDX creates Taxonomy based on Reporting and Accounting Standards

Issuer

•Issuer input reporting information into the Instance Document

Instance Document

create Output

22

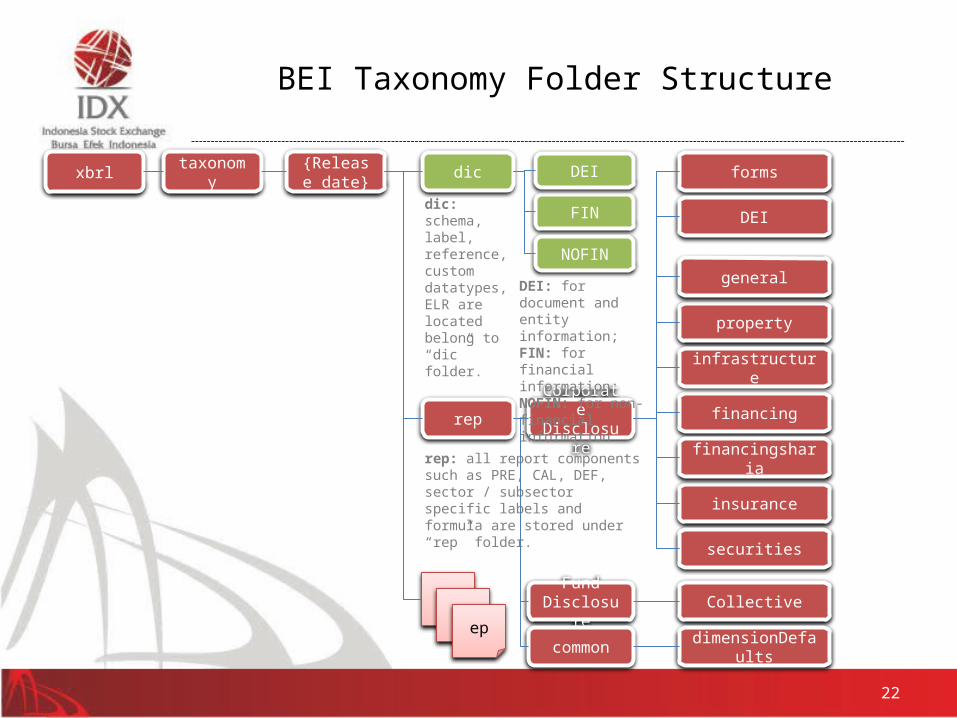

BEI Taxonomy Folder Structure

{Release date}

dic

rep

FIN

DEI

NOFIN

forms

insurance

DEI

CorporateDisclosure

epep

ep

dic: schema, label, reference, custom datatypes, ELR are located belong to “dic” folder.

rep: all report components such as PRE, CAL, DEF, sector / subsector specific labels and formula are stored under “rep” folder.

DEI: for document and entity information; FIN: for financial information; NOFIN: for non-financial information

securities

property

financing

general

infrastructure

taxonomyxbrl

FundDisclosure Collective

financingsharia

common dimensionDefaults

Explanations on IDX Taxonomy

23

DEI

1. General

2. Property

3. Infrastructure

4. Finance & Sharia

5. Securities

6. Insurance

7. Collective

8. Financing

IDX Taxonomy

DEI

1. Statement of Financial Position

2. Statement of Comprehensive

Income3. Statement of

Changes in Equity

4. Statement of Cash Flow

References in IDX Taxonomy

The overall format of the financial statements which have been prepared, has been through a review process by taking samples on 188 listed company’s financial statement in IDX, or representing 35% of all listed companies.

Proposed IDX Taxonomy 2014 built by using several references and rules as follow:• Statement of Financial Accounting Standards (PSAK);• Statement of Sharia Accounting Standards;• Provision on Capital Market rule:

BAPEPAM-LK Rule No. VIII.G.7 about The Guidelines of Financial Report Presentation; BAPEPAM-LK Rule No. VIII.G.17 about The Accounting Guidelines of Securities

Companies; BAPEPAM-LK Circular Letter No. SE-17/BL/2012 about checklist of Financial Statement

Disclosure for All Industries in Indonesia Capital Market.

The references are the provision that applied in December 31, 2013 and will be applied in January 1, 2015.

24

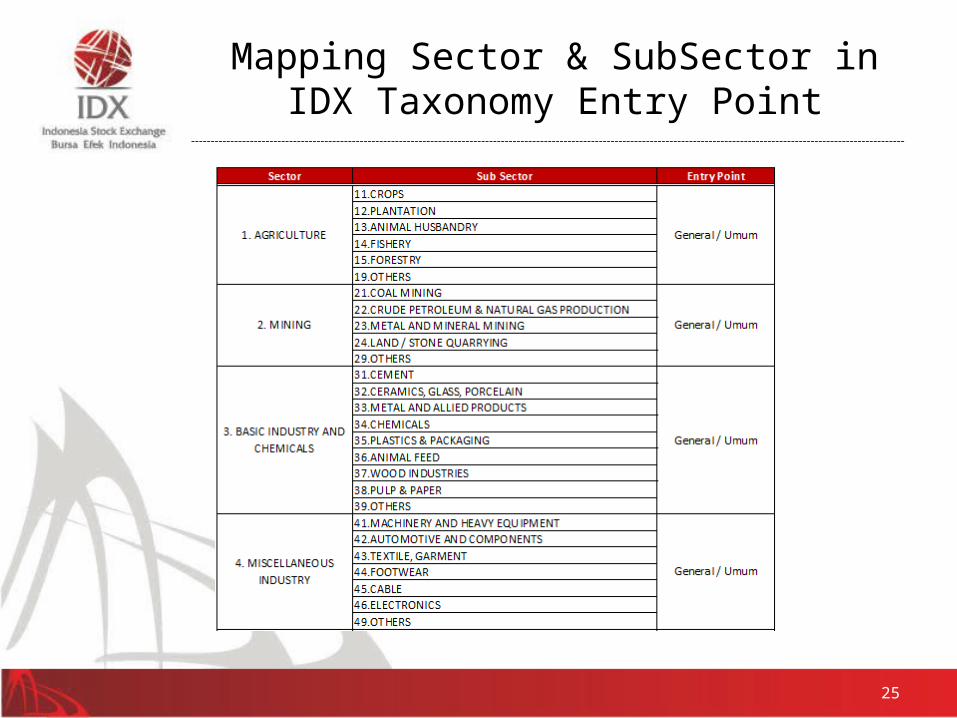

Mapping Sector & SubSector in IDX Taxonomy Entry Point

25

Mapping Sector & SubSector in IDX Taxonomy Entry Point - Continued

26

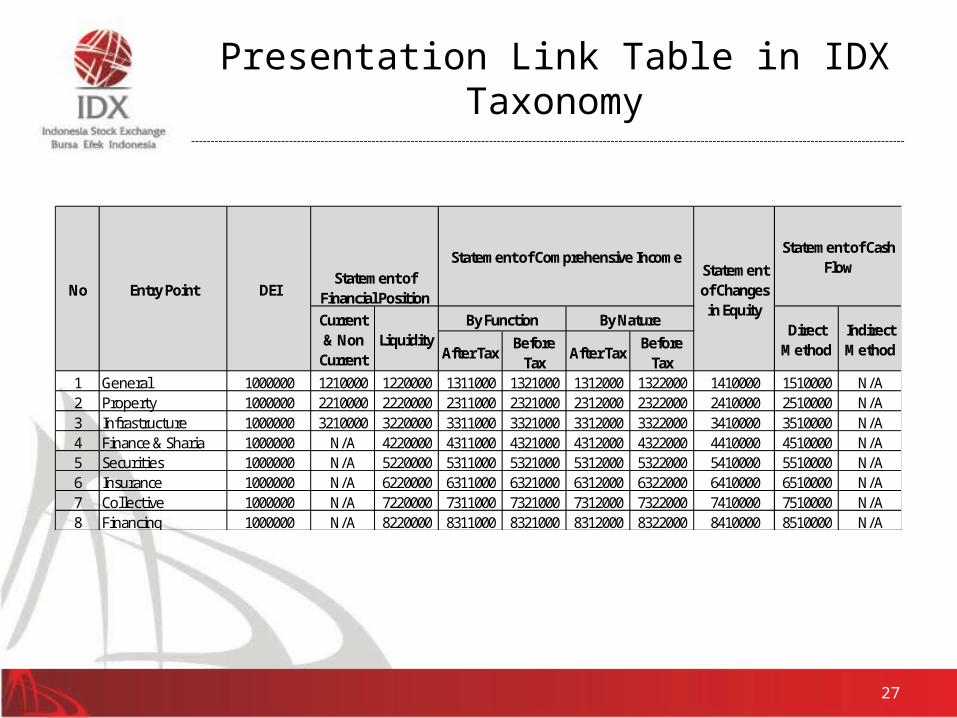

Presentation Link Table in IDX Taxonomy

27

After TaxBefore

TaxAfter Tax

Before Tax

1 General 1000000 1210000 1220000 1311000 1321000 1312000 1322000 1410000 1510000 N/A2 Property 1000000 2210000 2220000 2311000 2321000 2312000 2322000 2410000 2510000 N/A3 Infrastructure 1000000 3210000 3220000 3311000 3321000 3312000 3322000 3410000 3510000 N/A4 Finance & Sharia 1000000 N/A 4220000 4311000 4321000 4312000 4322000 4410000 4510000 N/A5 Securities 1000000 N/A 5220000 5311000 5321000 5312000 5322000 5410000 5510000 N/A6 Insurance 1000000 N/A 6220000 6311000 6321000 6312000 6322000 6410000 6510000 N/A7 Collective 1000000 N/A 7220000 7311000 7321000 7312000 7322000 7410000 7510000 N/A8 Financing 1000000 N/A 8220000 8311000 8321000 8312000 8322000 8410000 8510000 N/A

Statement of Cash Flow

By NatureBy Function

DEIEntry PointNo

LiquidityCurrent & Non

Current

Indirect Method

Direct Method

Statement of Changes

in Equity

Statement of Comprehensive IncomeStatement of

Financial Position

Sample Chart of Accounts (COA)

28

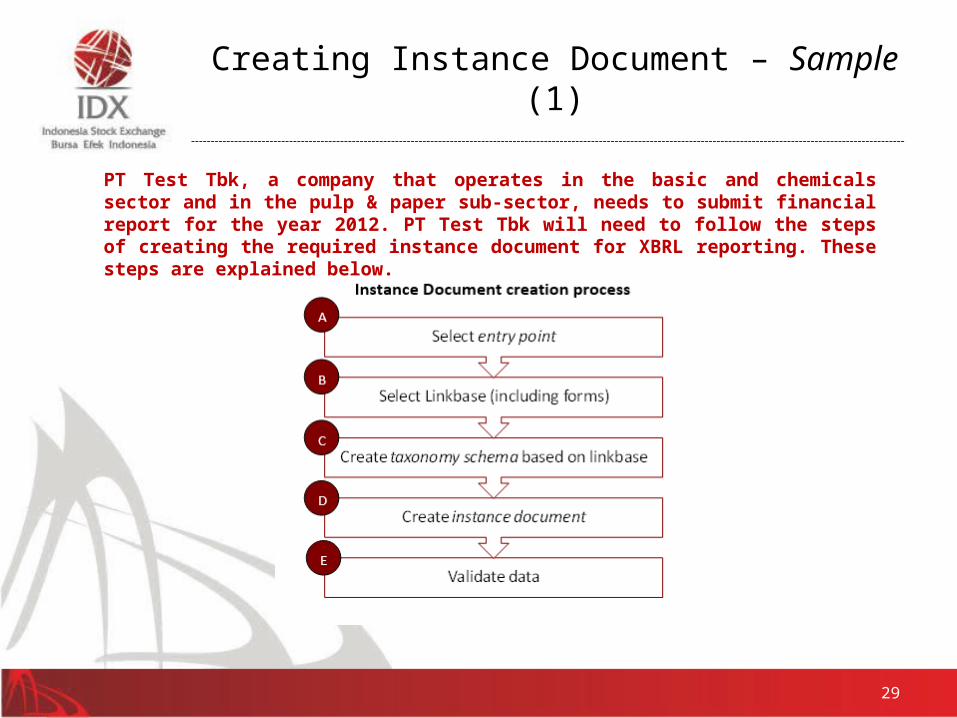

Creating Instance Document – Sample (1)

29

PT Test Tbk, a company that operates in the basic and chemicals sector and in the pulp & paper sub-sector, needs to submit financial report for the year 2012. PT Test Tbk will need to follow the steps of creating the required instance document for XBRL reporting. These steps are explained below.

Creating Instance Document – Sample (2)

30

Select entry pointA

Sample of entry point PT Test Tbk

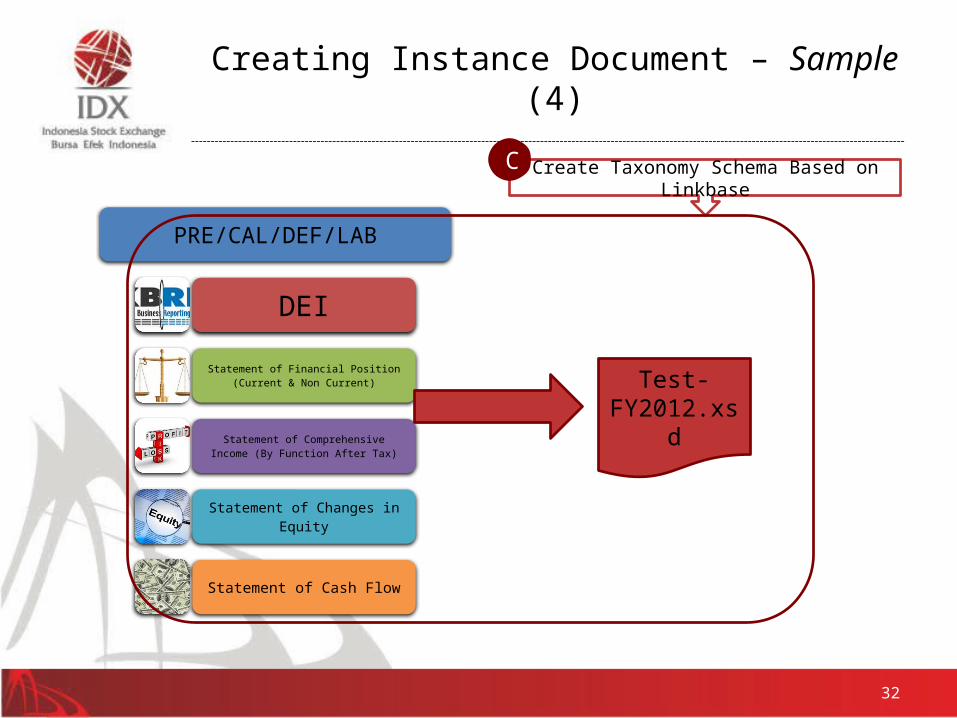

Creating Instance Document – Sample (3)

31

Select linkbase (including form)B

After TaxBefore

TaxAfter Tax

Before Tax

1 General 1000000 1210000 1220000 1311000 1321000 1312000 1322000 1410000 1510000 N/A2 Property 1000000 2210000 2220000 2311000 2321000 2312000 2322000 2410000 2510000 N/A3 Infrastructure 1000000 3210000 3220000 3311000 3321000 3312000 3322000 3410000 3510000 N/A4 Finance & Sharia 1000000 N/A 4220000 4311000 4321000 4312000 4322000 4410000 4510000 N/A5 Securities 1000000 N/A 5220000 5311000 5321000 5312000 5322000 5410000 5510000 N/A6 Insurance 1000000 N/A 6220000 6311000 6321000 6312000 6322000 6410000 6510000 N/A7 Collective 1000000 N/A 7220000 7311000 7321000 7312000 7322000 7410000 7510000 N/A8 Financing 1000000 N/A 8220000 8311000 8321000 8312000 8322000 8410000 8510000 N/A

Statement of Cash Flow

By NatureBy Function

DEIEntry PointNo

LiquidityCurrent & Non

Current

Indirect Method

Direct Method

Statement of Changes

in Equity

Statement of Comprehensive IncomeStatement of

Financial Position

11 22 33 44 55

PRE/CAL/DEF/LAB

DEIStatement of Financial Position

(Current & Non Current)

Statement of Comprehensive Income (By Function After Tax)

Statement of Changes in Equity

Statement of Cash Flow

32

Create Taxonomy Schema Based on LinkbaseC

Test-FY2012.xsd

Creating Instance Document – Sample (4)

33

Creating Instance Document – Sample (5)

Create Instance DocumentD

34

Creating Instance Document – Sample (6)

Validate DataE

Creating Instance Document – Sample (7)

Formula Validation • Existence Validation

Obligation to fill selected account in the financial statement.Example: Current Asset, Non Current Asset, Total Asset, Total Equity, etc.

• Assertion ValidationInterconnection validation of certain account in financial statement. Example: Cash balance in the Statement of Financial position must be equal with Ending Cash balance in the Cash Flow Statement.

35

36

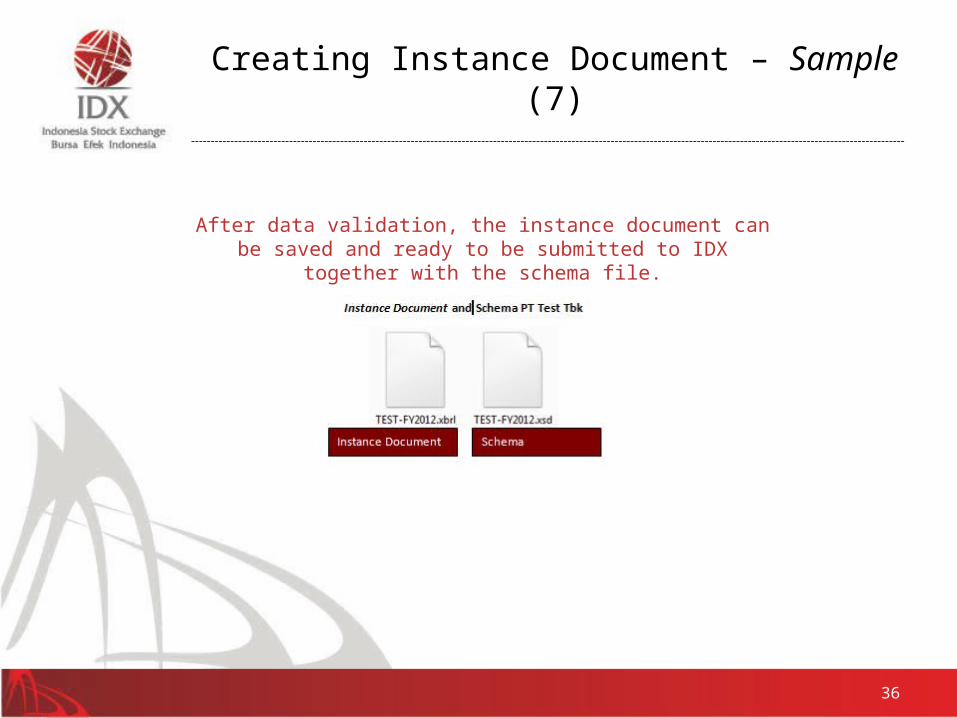

Creating Instance Document – Sample (7)

After data validation, the instance document can be saved and ready to be submitted to IDX together with the schema file.

37

Feedback

Purpose of Socialization

• Introducing IDX Taxonomy and its development planning

• To obtain public reviews and feedback for IDX Taxonomy from Listed Companies

38

Planning After Feedback

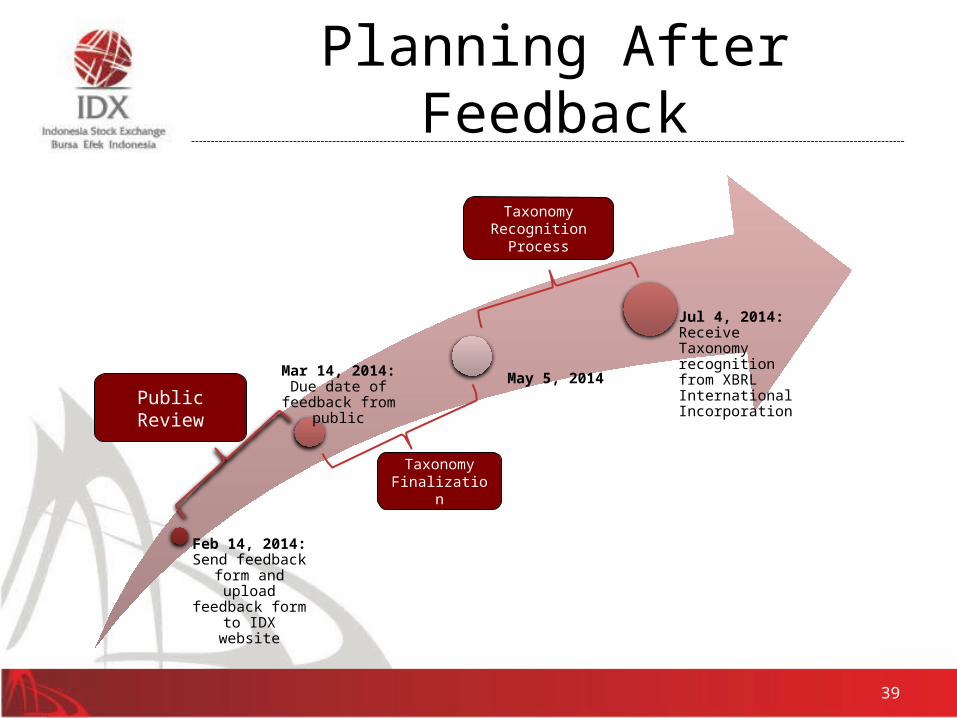

Feb 14, 2014: Send feedback form and

upload feedback form to IDX website

Mar 14, 2014: Due date of feedback from public May 5, 2014

Jul 4, 2014: Receive Taxonomy recognition from XBRL International Incorporation

39

Public Review

Taxonomy Finalization

Taxonomy Recognition Process

XBRL Information - Website

40

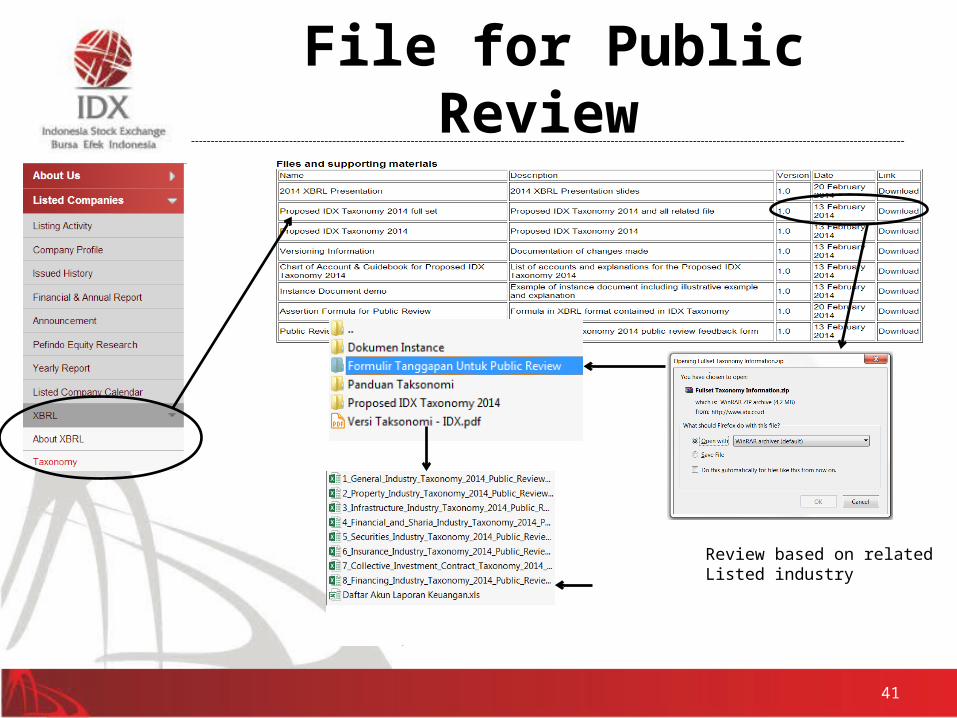

File for Public Review

Review based on related Listed industry

41

Guidance Public Review

1. Go to website : www.idx.co.id2. Download file from “XBRL taxonomy” “Files and supporting materials”

“Proposed IDX Taxonomy 2014 full set”3. Review Chart of Account4. Review Formula5. Fill the public review form6. Submit public review form via email to [email protected] no later than March

14, 2014

*) IDX will recap all feedback by the cut off date as part of the IDX Taxonomy refinement process. The updated taxonomy after the review process will become the standard reporting format for financial statements which will be submitted by Listed Companies to IDX through electronic reporting.

42

43

Requested for review

1. Chart of Account (Sample)2. Formula (Sample)

Form Feedback

44

Link

45

Thank You